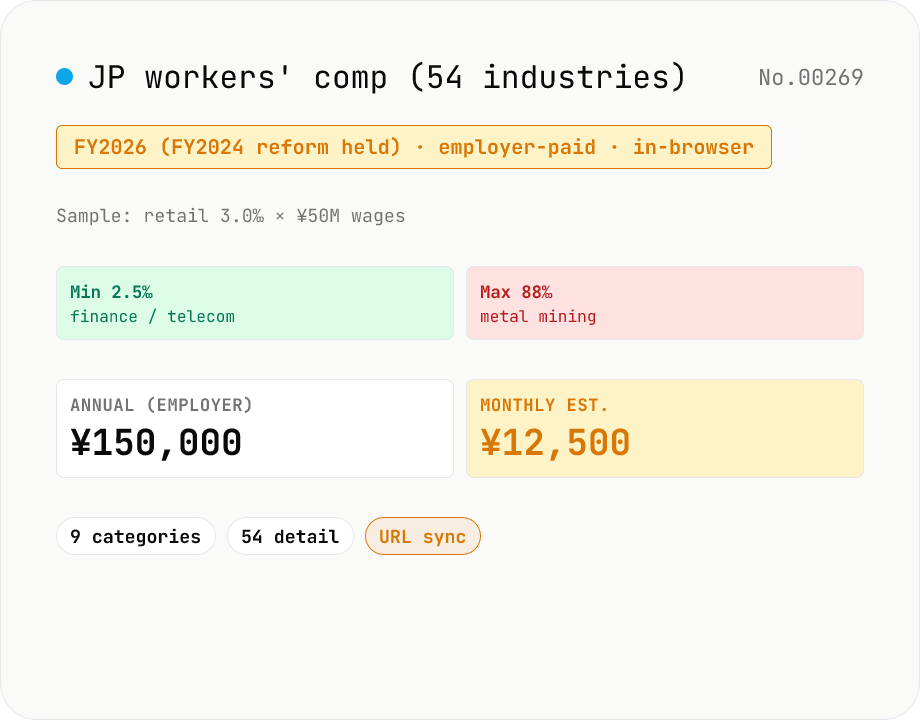

JP workers' compensation (rosai) premium — 54 industries × FY2026 rates

Estimate Japan's workers' compensation premium from annual gross wages × per-industry rate. 54 industries grouped into 9 categories, using the FY2024 reform rates (held for FY2025 and FY2026). Ranges from 2.5/1000 (finance, telecom) to 88/1000 (metal mining). Unlike employment insurance, rosai is fully employer-paid. Filed annually together with employment insurance as 'labour insurance'.

How to use

1) Pick the **industry category** (9 groups). 2) From the **detail** select (54 industries), choose your company's principal industry. 3) Enter the **annual gross wages** (April–March, bonuses included). Annual and monthly figures display automatically. Unlike employment insurance, rosai is fully employer-paid and never deducted from wages.

In depth

Industry category and payroll reveal business scale and sector

The two inputs — industry subcategory and annual gross wages — reconstruct the type of business and its approximate headcount or revenue range. A user entering ‘construction, other’ with ¥100M annual wages is describing a mid-size construction primary contractor with a recognisable labour-cost profile. That combination identifies a commercial target for occupational-injury insurance (労災上乗せ保険), safety-equipment suppliers, social insurance advisors (社会保険労務士), and HR outsourcing firms.

Workers’ compensation calculators offered by payroll-software vendors and labour-law advisory sites see their user base as employers and their payroll administrators — the people responsible for 年度更新 filing. Input data that reveals an employer’s industry and payroll scale is the entry point for sales of additional employer-facing products. A tool used for a quick cross-check before the June annual filing can produce a durable server record of a company’s approximate size and sector.

54 industry rates as JavaScript constants — no lookup required

Workers’ compensation rates are statutory constants revised every three years by MHLW based on industry incident data. The post-FY2024 rates for all 54 industry subcategories — ranging from 2.5/1000 (finance / telecom / instruments) to 88/1000 (metal and coal mining) — are loaded as a JavaScript object at page load. The premium formula is simply annual_wages × rate. No server call is required at any point. The same rates apply through FY2025 and FY2026; the next revision is expected in FY2027. Open DevTools Network and change the industry or wage figure — nothing fires after the initial page load.

Merit rating: when the standard rate does not apply

Employers with 100 or more workers — or 20 to 100 workers meeting specific revenue thresholds — are subject to the merit rating system, which adjusts the standard rate by up to ±40% based on the past three years’ injury and illness record. Construction sites have a separate aggregate merit system. This tool uses standard rates only; the merit-adjusted rate appears on the labour-standards-office notification that accompanies the annual update filing. For employers subject to merit rating, use this tool as a rough benchmark and apply the notified rate for the actual filing calculation.

Annual update filing (June–July) and combining with employment insurance

Labour insurance (rosai + koyo) is filed and paid together at the annual 年度更新 from June 1 to July 10. The filing reconciles the prior-year actual premium (actual wages × rate) against the provisional payment made the previous year, then pays a new provisional premium for the current year. Running this tool for the rosai portion and koyo-hoken-jp for the employment-insurance employer share gives a combined labour-insurance estimate before the window opens. The separate social-insurance employer share (health + pension) is handled by kenpo-kyokai-jp — all three stay browser-only. For years with unusually high bonus payments that inflate total wages significantly above the prior year’s estimate, the reconciliation payment can be large.

Nine-category / 54-subcategory structure and the rate-revision rationale

Workers’ compensation rates are set under Workers’ Accident Insurance Act Article 32-3 based on the past three years of injury-incidence rates (per-mille: workplace casualties / average workforce × 1,000), revised every three years (source: MHLW rate-revision notice). The nine top-level categories are: (1) forestry 60/1000; (2) fisheries 9–18/1000; (3) mining 26–88/1000 (metal and coal highest); (4) construction 9–62/1000 (quarrying highest); (5) manufacturing 2.5–26/1000; (6) transport 4–9/1000; (7) electricity/gas 3/1000; (8) other — commerce, finance, communications — 2.5–13/1000; (9) ship-owner 47/1000. The spread between the lowest (finance, insurance, telecoms) and highest (metal mining) is about 35×.

The 54-subcategory split matters in practice; misclassification triggers labour-standards-office inquiries at the annual update. Within manufacturing, food processing (2.5/1000) is well below chemicals (4/1000) and metal products (10/1000). Construction breaks into civil engineering (16/1000), building work (9.5/1000), and existing-building equipment installation (12/1000), each with its own rate. This tool’s nine-category → 54-subcategory drill-down mirrors this hierarchy. Mixed businesses (e.g., manufacturing plus in-house delivery) should select the principal activity per MHLW notification — the dominant business categorisation governs.

Special enrolment for SME owners, sole-trader contractors, and overseas postings

The basic rosai system covers only ‘workers’ — owners, directors, and self-employed sole traders are excluded. A special enrolment regime covers owners and self-employed contractors whose work resembles employee labour closely enough to merit equivalent protection (source: MHLW special enrolment for workers’ comp). SME-owner special enrolment is available for businesses with up to 300 employees (50 for finance, insurance, real-estate, retail; 100 for service businesses), enrolled through a labour-insurance administrative association (労働保険事務組合). The owner can self-select a benefit basis amount of JPY 3,500–25,000 per day, with the rate applied being the standard rosai rate for the industry.

Construction sole-trader contractors — independent carpenters, plasterers, others working without employees — enrol via a union or administrative association at a standard 18/1000. Overseas-posting special enrolment covers Japanese employees seconded abroad, with the home-country employer handling enrolment. These special premiums are outside this tool’s scope; quotes come from the relevant administrative association or union. The cost-benefit case for special enrolment is strong — premiums run a few tens of thousands of yen annually while injury or fatality benefits reach the millions or tens of millions, so eligible owners and self-employed contractors are typically advised to enrol.

FAQ

- Is this deducted from my paycheck?

- **No**. Workers' compensation is **fully employer-paid** and normally does not appear on the payslip. Employment insurance is shared (employee 5/1000 + employer 8.5/1000 for general business) and is deducted. Rosai is only on the employer side, filed annually together with employment insurance as 'labour insurance'.

- Why does the rate differ so much by industry?

- Because injury rates differ massively. Lowest: **finance / insurance / real estate, telecom / broadcasting, instruments, oil & gas = 2.5/1000**. Highest: **metal / non-metal / coal mining = 88/1000** (~35× gap). Forestry 52, shipbuilding 23, set-net fishery 37 are also high. MHLW reviews the rates every **3 years** based on the last 3 years' incident data per industry.

- What changed in the FY2024 revision?

- From April 2024, the industry-average dropped 4.5/1000 → 4.4/1000. Of 54 industries, **17 went down, 3 went up**, the rest held. Down: forestry (60→52), food (6→5.5), wood (14→13). Up: a few small ones. The rates loaded here are post-reform, and apply unchanged through FY2025 and FY2026.

- What is the construction 'labour cost ratio'?

- Primary-contractor construction can't easily report wages directly, so wages are estimated as contract value × **labour cost ratio**. E.g. general construction = 23%, rate 15/1000 → ¥10M contract × 23% × 15/1000 = ¥34,500. This tool assumes direct-hire wages; multiply by the labour ratio yourself for contract-based estimates.

- What is 'merit rating'?

- A ±40% surcharge / discount based on incident history. Applies to sites with 100+ workers, or 20-100 with conditions. 3 years of low incidents → up to 40% off; high incidents → up to 40% on. Construction also has 'aggregated merit' for fixed-term sites. This tool uses standard rates; merit not applied.

- Do small-employers / sole-traders qualify?

- Rosai normally covers **employees** for work-related injuries; sole-traders are out by default. Small-employers (≤ 300 workers; ≤ 50 for finance / insurance / real estate / retail) and sole-traders (construction, transport, etc.) can opt into **special enrolment** to cover themselves: basic daily (¥3,500-¥25,000) × 365 × industry rate. Not handled here.

- Do foreign trainees / part-timers qualify?

- **Yes — all workers regardless of employment form** (full-time, part-time, contract, dispatched, foreign trainees, daily). No weekly-hour threshold like employment insurance. Coverage starts on day 1; the employer must register and pay the premium from the first day.

- What is 'annual update' (nendo-koshin)?

- From **Jun 1 to Jul 10** each year, employers settle 'labour insurance' (rosai + employment) at the Labour Standards Office (or e-Gov online). Files prior-year **actual** premium (actual wages × rate) and pays current-year **provisional** premium (estimated wages × rate). Missing the deadline incurs a **10% surcharge**.

- Difference from other social-insurance tools?

- This tool = only rosai (work-injury fund). Health + welfare pension + long-term care = kenpo-kyokai-jp. Employment insurance = koyo-hoken-jp. NHI (self-employed) = kokuho-hoken-jp. Class-1 long-term care (age 65+) = kaigo-hoken-jp. Combine kenpo-kyokai-jp + koyo-hoken-jp + rosai-hoken-jp for an office worker's full social-insurance picture.

- Is anything uploaded?

- No. All math runs in your browser, no network traffic.

How to verify nothing is uploaded

This tool never sends your input outside your browser. The pages below explain how it works, how to audit it, and how the site is run.

Related tools

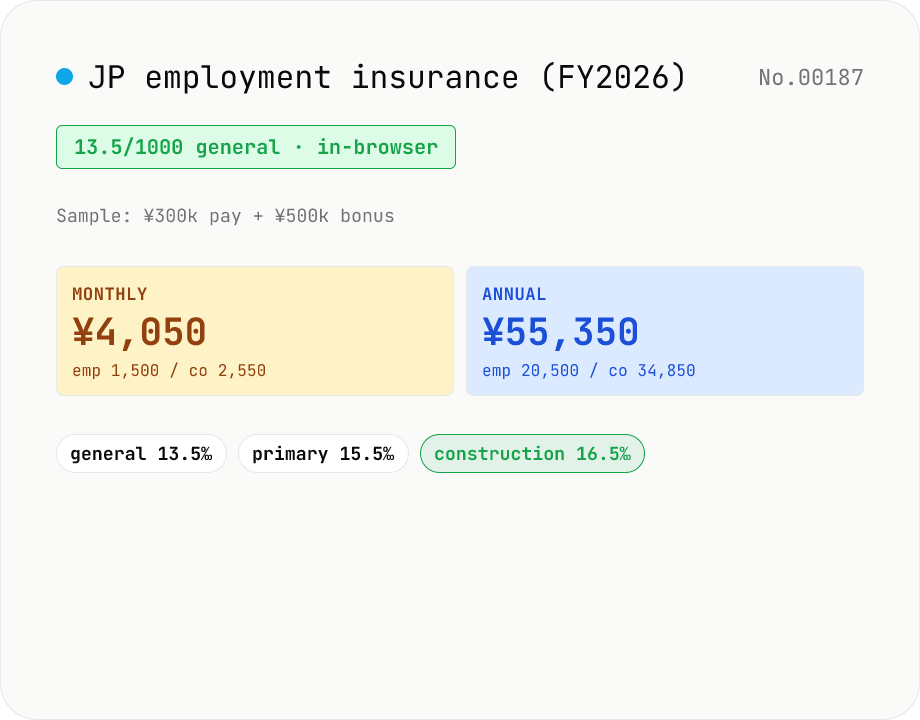

JP employment insurance premium — FY2026 rates × 3 industries (general / primary / construction)

Estimate Japan's employment insurance premium from monthly pay + bonus using FY2026 (Apr 2026 – Mar 2027) rates, split into employee + employer (incl. job-stability + skill-development levies). General 13.5/1000, agriculture/forestry/fishery/sake 15.5/1000, construction 16.5/1000 — pick via mode toggle. Only the employee share is deducted from pay. Runs entirely in your browser.

JP Kyokai-kenpo social-insurance simulator — prefecture-level + bonus

Estimate Japan's Kyokai-kenpo (national health insurance association) health + long-term care + welfare pension + the new FY2026 child-care support levy from monthly pay and bonuses, split 50/50. Covers all 47 prefecture rates and both 50-tier health / 32-tier pension grade tables. Runs entirely in your browser.

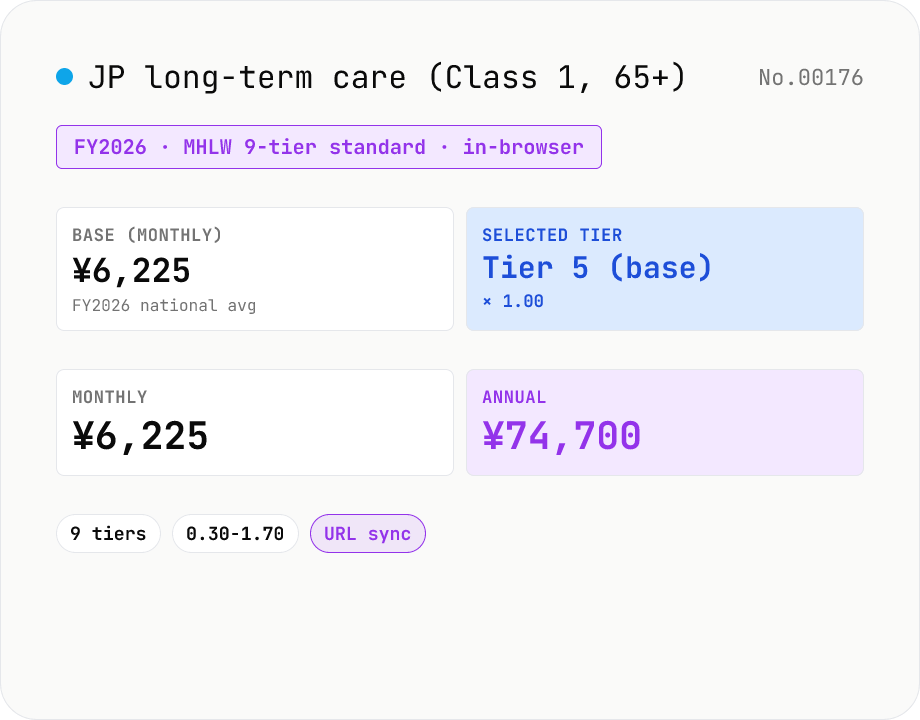

JP long-term care premium for age-65+ (kaigo-hoken Class 1) — 9 tiers × municipal base

Estimate Japan's long-term care insurance premium for Class-1 insured (age 65+) using the MHLW 9-tier standard and a municipal base amount. Defaults to the FY2026 national average base of ¥6,225 / month; pick your tier (multipliers 0.30–1.70) for an annual + monthly figure. Includes a tier-selection hint table based on resident-tax status / pension income / aggregate income. Runs entirely in your browser.

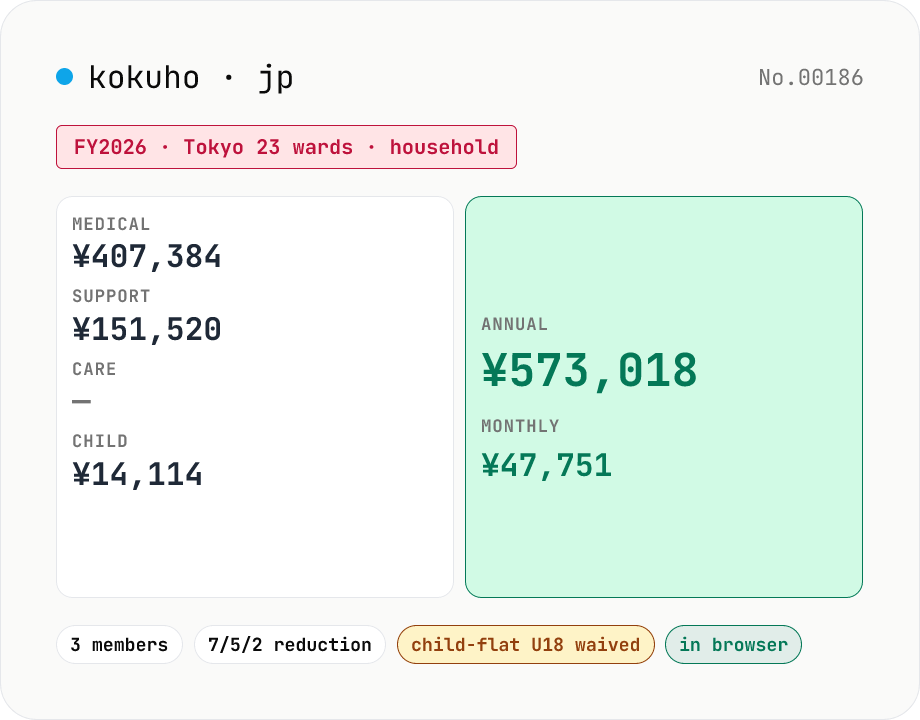

JP National Health Insurance simulator — household + reductions

Estimate Japan's National Health Insurance (kokuho) premium for FY2026 across the 4 categories (medical / support / care / child-care). Auto-applies 7/5/2 reductions and pre-school / under-18 carve-outs. Tokyo 23-ward preset + custom municipal rates. Runs entirely in your browser.