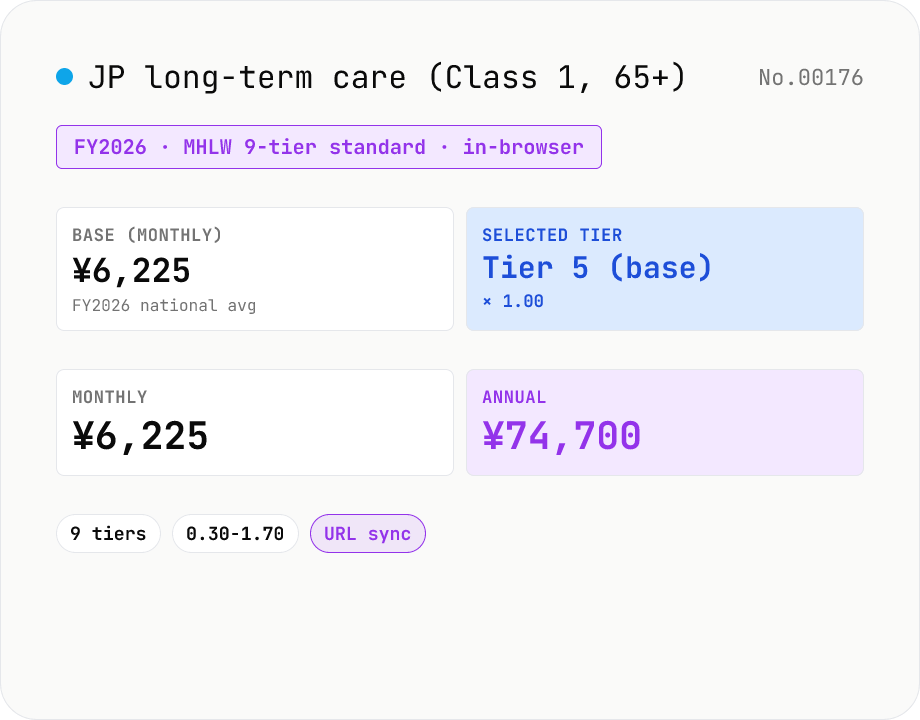

JP long-term care premium for age-65+ (kaigo-hoken Class 1) — 9 tiers × municipal base

Estimate Japan's long-term care insurance premium for Class-1 insured (age 65+) using the MHLW 9-tier standard and a municipal base amount. Defaults to the FY2026 national average base of ¥6,225 / month; pick your tier (multipliers 0.30–1.70) for an annual + monthly figure. Includes a tier-selection hint table based on resident-tax status / pension income / aggregate income. Runs entirely in your browser.

How to use

1) Enter the **base amount** (tier-5 monthly) for your municipality (default = ¥6,225 = FY2026 national average). 2) Pick your **tier (1-9)** using the criteria hint table (depends on household / individual resident-tax status, pension income, aggregate income). 3) The monthly / annual amount, multiplier, and payment method (special vs ordinary collection) update automatically. URL syncs with state for bookmarking / sharing.

In depth

Long-term care premium tiers reveal age, pension income, and tax status

Calculating a Class-1 (age 65+) long-term care insurance premium requires knowing the household and individual resident-tax status, pension income, and aggregate income — inputs that together identify age bracket, pension level, and income tier. This information is commercially valuable to providers of insurance products, elder-care services, and retirement financial planning, all of which target the 65+ demographic.

Beyond commercial targeting, the combination of ‘resident-tax-exempt household’ plus income level is a sensitive welfare indicator. It can signal eligibility for various public support programmes, and is the kind of data that deserves at minimum the same protection as medical information.

Why elder-care financial tools should not send data to servers

Care-insurance calculators appear on the websites of elder-care facilities, life insurers, and regional banks — all of whom have a direct commercial interest in identifying the income level and care-payment capacity of prospective clients. Entering age, pension income, and resident-tax status into a server-side form on one of these sites connects that data to their CRM, even if no account is created.

The calculation itself is one multiplication — base amount × tier multiplier — which JavaScript executes instantly in your browser. No server is needed.

Municipality-specific base amount with in-browser arithmetic

The tool multiplies the tier-5 monthly base amount (default ¥6,225 = FY2026 national average) by the MHLW-standard tier multipliers (0.30 to 1.70 for tiers 1–9, post-subsidy rates for tiers 1–3). The base amount field is editable so you can enter the exact figure from your municipality’s notification letter. The payment method (special-collection from pension / ordinary-collection by slip) is flagged automatically. Nothing reaches a server.

URL state-sync means you can bookmark the result for your specific tier and base amount, then recheck next year when the base amount is revised.

When to use this estimate and when to look at the actual notice

Many municipalities have extended beyond the standard 9 tiers to 13–17 to capture higher-income households, and some have custom multipliers above 1.70. This tool uses the standard 9-tier model, so if you are in a higher tier the actual premium will be more than shown here. The definitive figure is on the premium notice mailed by your municipality each July. Use this tool to understand the structure and approximate the amount, then verify against the notice for the exact payment. For Category-2 insured (ages 40–64), the care premium is bundled with health insurance — kenpo-kyokai-jp handles employees and kokuho-hoken-jp handles NHI-side cases — both stay browser-only.

The nine-tier structure, the three-year revision cycle, and the 9th Plan (FY2024 onward)

Japan’s long-term care insurance operates on a three-year planning cycle under LTC Insurance Act Article 117 (source: MHLW long-term care insurance plan). The current plan is the 9th (FY2024–FY2026), with a FY2026 national-average base of JPY 6,225 per month (tier 5). Each municipality builds its own plan from projected service demand and the elderly-population mix. The 8th plan (FY2021–FY2023) averaged JPY 6,014; the 9th rose 3.5%, reflecting growing elderly population and care demand.

The nine tiers run from tier 1 (welfare recipients or resident-tax-exempt households with pension income ≤ JPY 800k) at 0.30× the base, through tier 5 (the reference) at 1.00, to tier 9 (taxable households with aggregate income ≥ JPY 3M) at 1.70. The detailed boundaries: tier 2 is non-taxable households with pension JPY 800k–1.2M at 0.50; tier 3 is non-taxable above JPY 1.2M at 0.70; tier 4 is taxable household but individually non-taxable at 0.90; tier 6 is individually taxable with aggregate income < JPY 1.2M at 1.20; tier 7 is JPY 1.2M–2M at 1.30; tier 8 is JPY 2M–3M at 1.50. This tool implements these multipliers as JavaScript constants, with tiers 1–3 already reflecting the FY2024 enhanced-reduction rates after the reform.

Municipal expansion beyond nine tiers and the special-vs-ordinary collection rules

Many of Japan’s special wards (Tokyo’s 23-ku), designated cities, and core cities have extended above the standard nine tiers — up to 13 to 17 tiers — to capture higher-income households. Tokyo Shinjuku-ku’s FY2026 schedule uses 17 tiers, with the top tier (aggregate income ≥ JPY 15M) at a multiplier of 3.30 (roughly double this tool’s 1.70 cap), yielding about JPY 250k per year. Areas with concentrated high earners typically have more tiers and steeper top-tier rates. Because this tool uses the standard nine-tier model, anyone falling into tier 9 should verify against the actual municipal notice — the real figure is likely higher.

Collection method defaults to ‘special collection’ (deducted from pension payments) for those receiving annual pension above JPY 180k. The premium is withheld six times per year on the even-numbered months when pension payments arrive. Recipients below JPY 180k of annual pension, or those whose special collection is interrupted by relocation or pension suspension, are switched to ‘ordinary collection’ — paper bills (typically eight instalments from July through the following March) or bank auto-debit. Category-2 insured (ages 40–64) pay their long-term care premium bundled with their health insurance premium and are outside this tool’s scope. For Category-2 calculations, use kenpo-kyokai-jp (employees) or kokuho-hoken-jp (NHI).

FAQ

- Difference between Class 1 and Class 2 insured?

- **Class 1**: Age 65+. Set by each municipality. *This tool*. **Class 2**: Age 40-64. Employees add to Kyokai-kenpo / kempo-kumiai health premium (FY2026 = 1.62%); self-employed add to NHI premium. See kenpo-kyokai-jp / kokuho-hoken-jp to compute those.

- 9 tiers vs 13 tiers?

- MHLW standard = **9 tiers** (1-9). Many municipalities add tiers 10-13+ to put more burden on higher earners (the 2024 reform strongly encourages 13+). Tokyo 23 wards often use 13-17 tiers, designated cities typically 15-17. This tool uses the standard 9-tier model, so high earners may see an under-estimate.

- How are the multipliers (0.30-1.70) decided?

- MHLW standard: 1=0.30 / 2=0.50 / 3=0.70 / 4=0.90 / 5=1.00 (base) / 6=1.20 / 7=1.30 / 8=1.50 / 9=1.70. Tiers 1-3 are subsidised by national / prefectural / municipal funds; the shown multipliers are post-subsidy (FY2026). Many municipalities customise multipliers for tier 6+, so always check your local figures.

- What does 'aggregate income' / 'taxable pension income' mean?

- **Aggregate income**: pension + salary + business + property income, before deducting carried-over losses (i.e., before various deductions). **Taxable pension income**: public pension income (old-age, retirement). Survivor / disability pensions are tax-exempt and not counted. Each year's classification is finalised in July based on the previous year's income.

- Why ask the user for the base amount?

- Base amounts are set per municipality on a 3-year cycle. For FY2024-2026, Tokyo 23 wards run ¥7,000-8,000, regional cities ¥5,000-6,500. We default to the national average of ¥6,225; for precision, use the value from your municipality's April 2024 notification.

- Special vs ordinary collection?

- **Special collection** (pension deduction): if monthly pension ≥ ¥15,000 (annual ≥ ¥180,000), auto-deducted bi-monthly. **Ordinary collection** (slip / bank transfer): for low-pension or no-pension recipients. Usually split into 6-10 instalments per year. Tool shows annual; divide by 12 (monthly) or by 6 (bi-monthly special) for each instalment.

- What about people turning 65 mid-year?

- Class-1 starts in the month containing the day before your birthday (e.g. born 1 May → starts April). The year is prorated by the number of qualifying months. This tool reports annual, so divide by 12 and multiply by remaining months (e.g. start Nov → annual / 12 × 5 for Nov-Mar).

- What happens if I don't pay?

- 1 year late → pay 100% out of pocket for services and claim a refund. 1.5 years → benefits suspended. 2 years → claim expires; copay rises from 10% → 30%. Special collection (pension deduction) prevents arrears automatically; ordinary collection requires self-discipline.

- Relation to 'high-cost care service fee'?

- This tool estimates premiums (paid monthly). The 'high-cost care service fee' caps your copay (10-30%) per month when receiving services; caps vary by household tax bracket (e.g. ¥44,400 for general households; ¥24,600 household / ¥15,000 individual for tax-exempt). Not handled here.

- Is anything uploaded?

- No. All math runs in your browser, no network traffic.

How to verify nothing is uploaded

This tool never sends your input outside your browser. The pages below explain how it works, how to audit it, and how the site is run.

Related tools

JP Kyokai-kenpo social-insurance simulator — prefecture-level + bonus

Estimate Japan's Kyokai-kenpo (national health insurance association) health + long-term care + welfare pension + the new FY2026 child-care support levy from monthly pay and bonuses, split 50/50. Covers all 47 prefecture rates and both 50-tier health / 32-tier pension grade tables. Runs entirely in your browser.

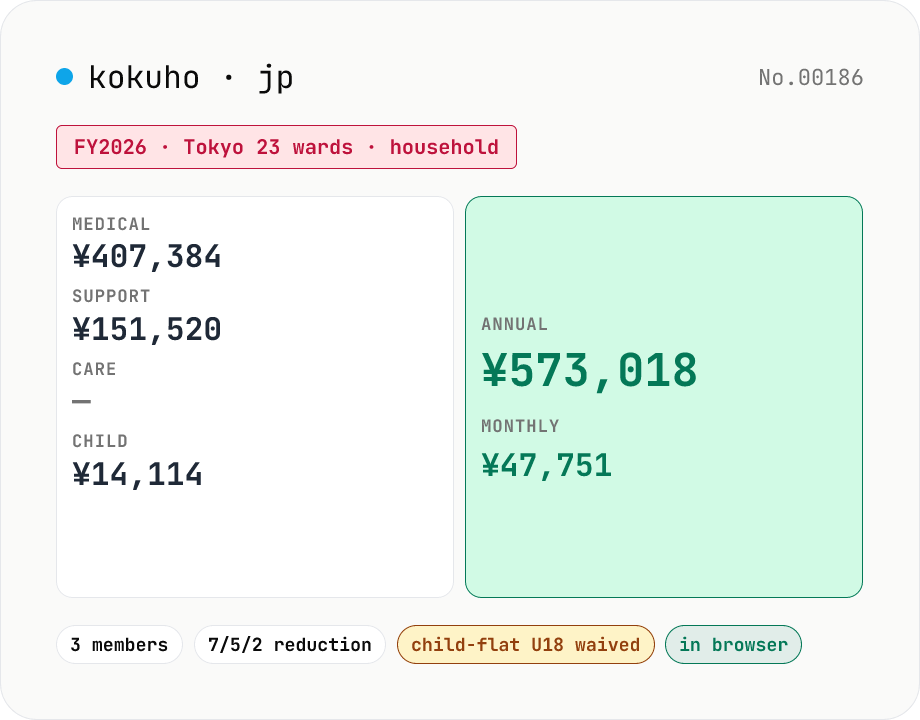

JP National Health Insurance simulator — household + reductions

Estimate Japan's National Health Insurance (kokuho) premium for FY2026 across the 4 categories (medical / support / care / child-care). Auto-applies 7/5/2 reductions and pre-school / under-18 carve-outs. Tokyo 23-ward preset + custom municipal rates. Runs entirely in your browser.

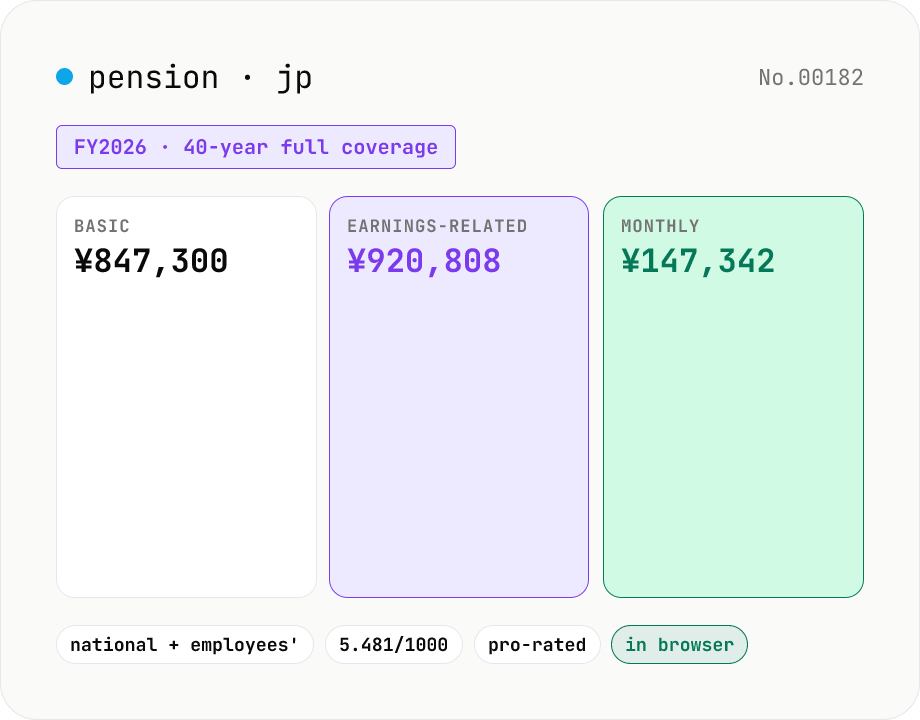

Japan pension estimator — basic + earnings-related (FY2026 figures)

Enter your accumulated months in the National Pension and the Employees' Pension, plus your average standard remuneration during the employees' pension period, to estimate the annual / monthly public pension you'll receive in retirement. Uses the FY2026 (令和 8 年度) full basic-pension figure of JPY 847,300/year (JPY 70,608/month) and the 5.481/1000 earnings-related multiplier (Heisei-15-and-later formula). Pro-rates by contributing months so partial careers (20–60 years of age, 25 / 30 / 35 years of coverage) work too. Runs entirely in your browser — salary figures never leave the device.

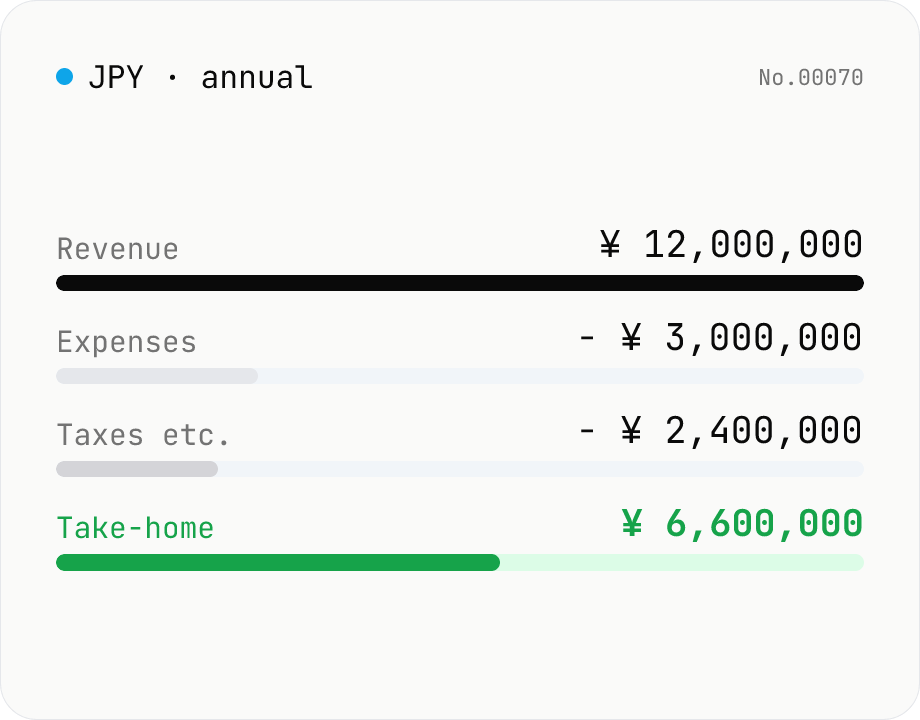

Japan Freelance Tax Calculator — Income, Resident, Health, Business Tax

Free online Japan freelance / sole-proprietor tax calculator. Annual estimator covering income tax, resident tax, consumption tax, national health insurance, business tax, and furusato-nozei cap. Useful for kojin jigyō nushi planning their year-end provisional tax. Runs entirely in your browser — figures never leave your device.