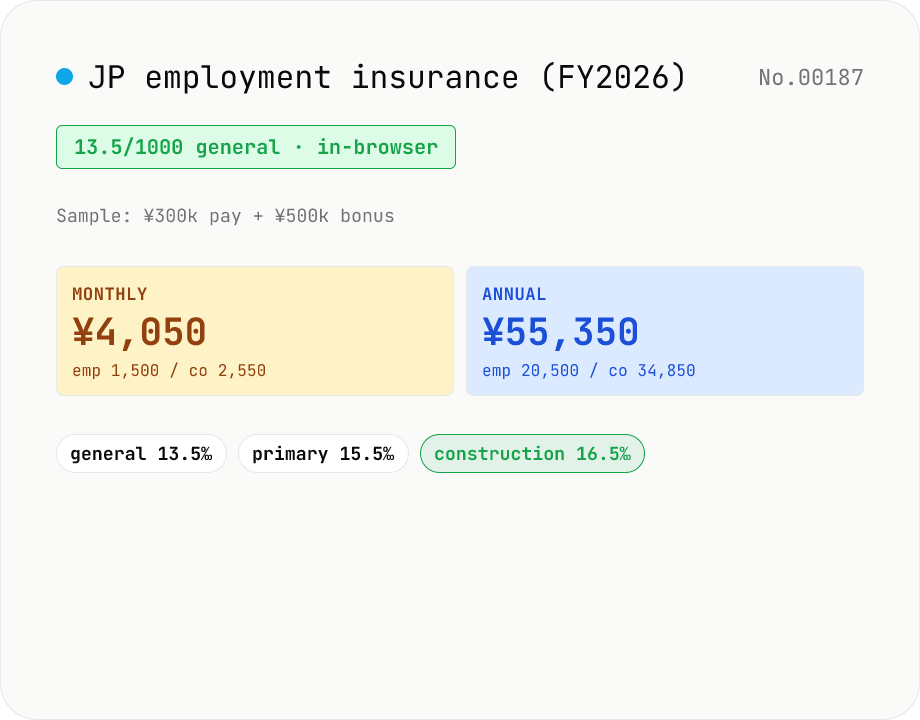

JP employment insurance premium — FY2026 rates × 3 industries (general / primary / construction)

Estimate Japan's employment insurance premium from monthly pay + bonus using FY2026 (Apr 2026 – Mar 2027) rates, split into employee + employer (incl. job-stability + skill-development levies). General 13.5/1000, agriculture/forestry/fishery/sake 15.5/1000, construction 16.5/1000 — pick via mode toggle. Only the employee share is deducted from pay. Runs entirely in your browser.

How to use

1) Pick the **industry** (general / agriculture-forestry-fishery-sake / construction). 2) Enter **monthly pay** (gross including overtime + commuting allowance) and **annual bonus**. 3) Monthly employee / employer shares, bonus-time deduction, and annual total update automatically. URL syncs with state for bookmarking / sharing.

In depth

Employment insurance inputs reveal salary, industry, and bonus structure

The three inputs — industry category, monthly pay, and annual bonus — together reconstruct annual gross salary and narrow the user’s occupational field. Construction vs general business signals the type of work. Monthly pay plus bonus reveals the income split and total annual compensation. That profile is useful to recruiters, headhunters, and financial advisors who want to identify individuals in specific salary bands.

Employment-insurance calculators appear on HR tech platforms and payroll service sites, which have a natural interest in connecting income data to their recruitment or advisory pipelines. Using a browser-side tool keeps your salary figures off those platforms.

A fixed-rate arithmetic problem that belongs entirely in your browser

FY2026 employment-insurance rates are statutory constants: general business 13.5/1000 total (employee 5/1000, employer 8.5/1000); primary industries 15.5/1000; construction 16.5/1000. The premium is wage × rate, computed separately for monthly pay and bonuses (no bonus cap, unlike health and pension insurance). No server lookup is needed — the rates don’t change mid-year, and they are publicly available from MHLW.

This tool embeds the FY2026 rates as JavaScript constants. The Network tab stays empty after the initial page load regardless of what you enter.

FY2026 rate cut reflected in-browser, URL-synced for next year

The FY2026 cut (down 1‰ from FY2025, the second consecutive reduction) is reflected in the constants. Because the fiscal year for employment insurance runs April–March, the rates here apply from April 2026 through March 2027. When rates change again in April 2027, the tool will be updated — but the URL state-sync means you can bookmark your current settings and return to recheck when the new rates take effect.

From payslip check to annual labour-insurance update

Employees can use this tool to verify the employment-insurance line on their payslip — the employee share of 5/1000 (general business) should match. Employers preparing for the June–July 年度更新 can use it to estimate the annual labour-insurance premium (rosai + koyo combined), then add the workers’ comp figure from rosai-hoken-jp to get the full labour-insurance bill. For the bundled health + pension premium, kenpo-kyokai-jp handles that side — both stay browser-only. Note that bonuses have no cap in employment insurance — high bonus periods significantly increase the employer share.

Why industry rates differ and the rationale for the FY2026 cut

Employment insurance rates are set annually by MHLW notification under Employment Insurance Act Article 68. FY2026 (April 2026 – March 2027) rates are 13.5/1000 for general business, 15.5/1000 for primary industries and sake brewing, and 16.5/1000 for construction (source: MHLW rate-setting notice). The three-tier structure reflects historical claim ratios: primary industries have heavier seasonal and short-term employment patterns, and construction has higher workplace-injury and discharge rates than general business. The employer-employee split also varies by industry: general business runs employee 5/1000 / employer 8.5/1000 (gap 3.5); primary industries run employee 6 / employer 9.5 (gap 3.5); construction runs employee 6 / employer 10.5 (gap 4.5) — construction is the only sector where the employer carries a disproportionate share.

The FY2026 cut continues a downward trend, dropping rates 1‰ from FY2025 after the FY2024 cut of the same magnitude. The reduction reflects (1) the build-up of the employment insurance reserve fund (estimated at JPY 1.4T at end of FY2025) and (2) reduced spending after the COVID-19 employment-adjustment subsidy programme wound down. If the reserve fund erodes — due to a recession or another shock that triggers heavy unemployment-benefit payouts — rates adjust upward. This tool implements the FY2026 figures as JavaScript constants; an FY2027 update will require new constants after the spring 2027 notification.

Bonus uncapped, commuting allowance included, and edge cases for high earners

Unlike health insurance and pension insurance — which cap standard bonus and salary amounts — employment insurance has no cap on bonus amounts. The full bonus is included in the premium base. For a worker on JPY 10M annual gross with JPY 4M of bonus, the employee share is (6M + 4M) × 5/1000 = JPY 50,000/year and the employer share is (6M + 4M) × 8.5/1000 = JPY 85,000/year. The employer’s burden on high bonuses is much lighter than under the capped systems, but it grows linearly with compensation rather than plateauing.

Commuting allowances are included in the premium base for employment insurance, mirroring how they enter the standardised salary used for health and pension (source: MHLW employment-insurance premium calculation). Edge cases to handle separately: (1) corporate directors (取締役) are excluded as non-employees, though concurrently-employed directors with recognised employee status are partially in scope; (2) workers newly hired at age 65 or older are in scope but pay zero employee share (this special exemption, in force since FY2019, dropped the employee rate from 5/1000 to 0 for that group after the end of the High-Age Continued Employment Benefit programme); (3) part-time workers under 20 hours per week are out of scope. Employers who include any of these categories in the headcount when totaling wages will overpay at the annual update. Worker-level scope determination typically requires a labour-law consultant (社労士) or labour-management software.

FAQ

- Is this what's deducted from my payslip?

- Yes — the employment-insurance line on your payslip shows the employee share (5/1000 for general business). The employer pays the employer share (8.5/1000) separately, filed annually together with workers' comp as 'labour insurance' (one lump or 3 instalments).

- When does FY2026 apply?

- **1 April 2026 – 31 March 2027**. Down 1‰ from FY2025 (14.5/1000), the second consecutive reduction. Driven by improving finances of the unemployment-benefits fund.

- Why different rates for general / primary / construction?

- Reflects unemployment-risk differences. Construction has seasonal / project-cycle instability → highest (16.5/1000). Primary (weather risk) is middle (15.5/1000). General business (most office workers) = 13.5/1000. The 'two-business levy' (job stability + skill development, employer-only) is 4.5/1000 for construction vs 3.5/1000 elsewhere.

- Why does the employer pay more than the employee?

- **Unemployment benefits** (the joint fund for unemployment / childcare leave) are paid equally (5/1000 each in general business). The employer additionally bears the **two-business levy** (used for things like employment-adjustment subsidies), 3.5–4.5/1000. So the employer share ends up ~1.7-1.75× the employee's.

- Do bonuses count?

- Yes. Bonus × rate (e.g. 13.5/1000 for general). Unlike health / pension insurance, there is no cap on bonuses (a ¥10M bonus is fully subject). The tool shows 'bonus deduction (1 year)' as annual bonus × rate.

- Does part-time (under 20 hrs/week) qualify?

- Employment insurance requires **weekly hours ≥ 20** + **expected ≥ 31 days of employment**. Below that = not covered (no premium). Multi-job holders can combine two jobs since FY2022 with an opt-in.

- What about workers age 65+?

- Since April 2020, age-65+ workers are also subject (high-age insured). The previous exemption was abolished. Unemployment benefits for this group are paid as a 'high-age job-seeker lump sum' (no waiting period).

- What is the construction 'labour cost ratio'?

- Construction primary-contractors derive wage totals from contract value × **labour cost ratio** (e.g. 23% for general construction), then apply employment / workers' comp rates. This tool is for direct monthly-wage employees; primary-contract estimation isn't included (multiply by the 23% ratio manually).

- How to enrol with Hello Work?

- The employer files a **qualification notice** by the 10th of the month after hire, and a **loss-of-qualification notice** within 10 days of separation. The **separation slip** issued at exit is required for unemployment benefits — always collect it.

- Is anything uploaded?

- No. All math runs in your browser, no network traffic.

How to verify nothing is uploaded

This tool never sends your input outside your browser. The pages below explain how it works, how to audit it, and how the site is run.

Related tools

JP Kyokai-kenpo social-insurance simulator — prefecture-level + bonus

Estimate Japan's Kyokai-kenpo (national health insurance association) health + long-term care + welfare pension + the new FY2026 child-care support levy from monthly pay and bonuses, split 50/50. Covers all 47 prefecture rates and both 50-tier health / 32-tier pension grade tables. Runs entirely in your browser.

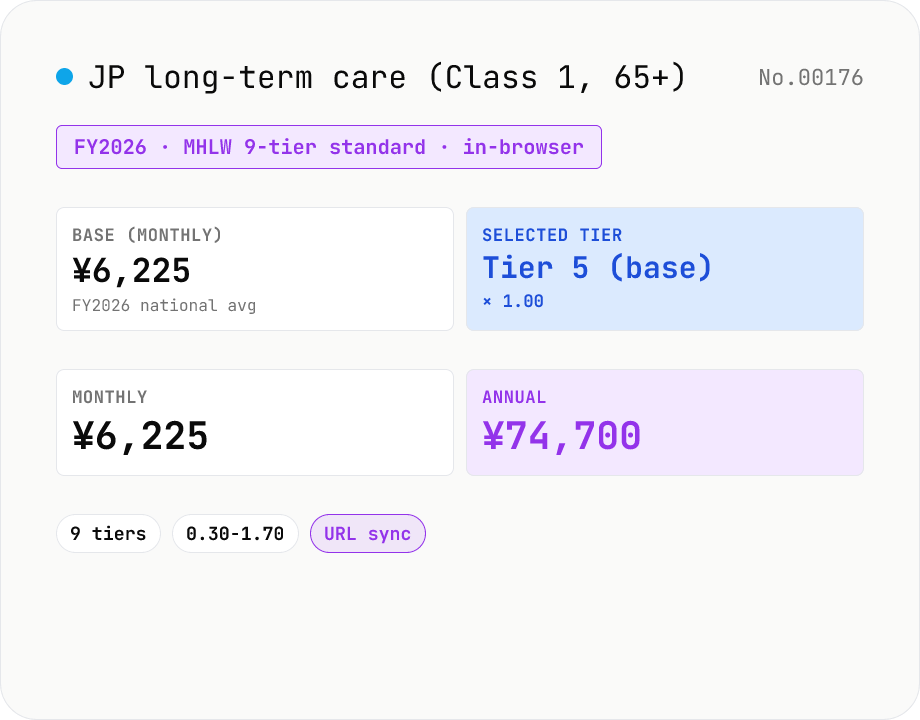

JP long-term care premium for age-65+ (kaigo-hoken Class 1) — 9 tiers × municipal base

Estimate Japan's long-term care insurance premium for Class-1 insured (age 65+) using the MHLW 9-tier standard and a municipal base amount. Defaults to the FY2026 national average base of ¥6,225 / month; pick your tier (multipliers 0.30–1.70) for an annual + monthly figure. Includes a tier-selection hint table based on resident-tax status / pension income / aggregate income. Runs entirely in your browser.

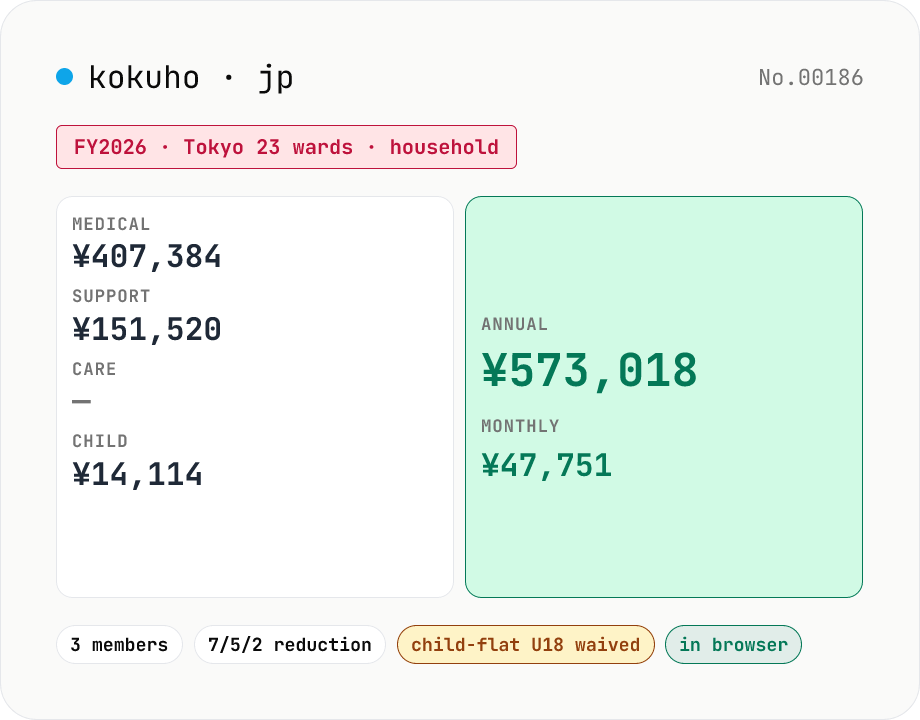

JP National Health Insurance simulator — household + reductions

Estimate Japan's National Health Insurance (kokuho) premium for FY2026 across the 4 categories (medical / support / care / child-care). Auto-applies 7/5/2 reductions and pre-school / under-18 carve-outs. Tokyo 23-ward preset + custom municipal rates. Runs entirely in your browser.

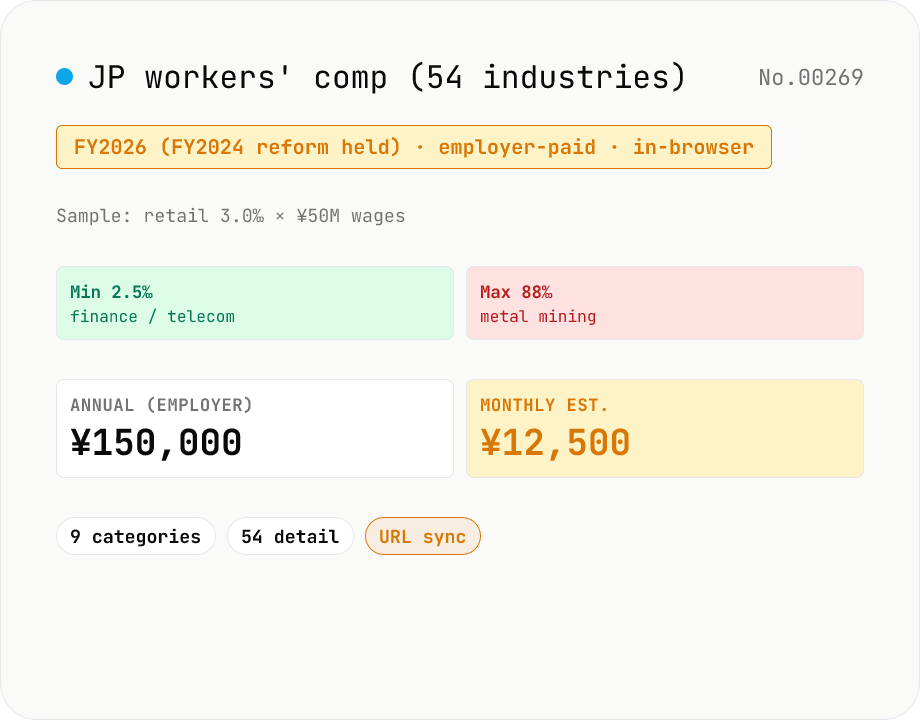

JP workers' compensation (rosai) premium — 54 industries × FY2026 rates

Estimate Japan's workers' compensation premium from annual gross wages × per-industry rate. 54 industries grouped into 9 categories, using the FY2024 reform rates (held for FY2025 and FY2026). Ranges from 2.5/1000 (finance, telecom) to 88/1000 (metal mining). Unlike employment insurance, rosai is fully employer-paid. Filed annually together with employment insurance as 'labour insurance'.