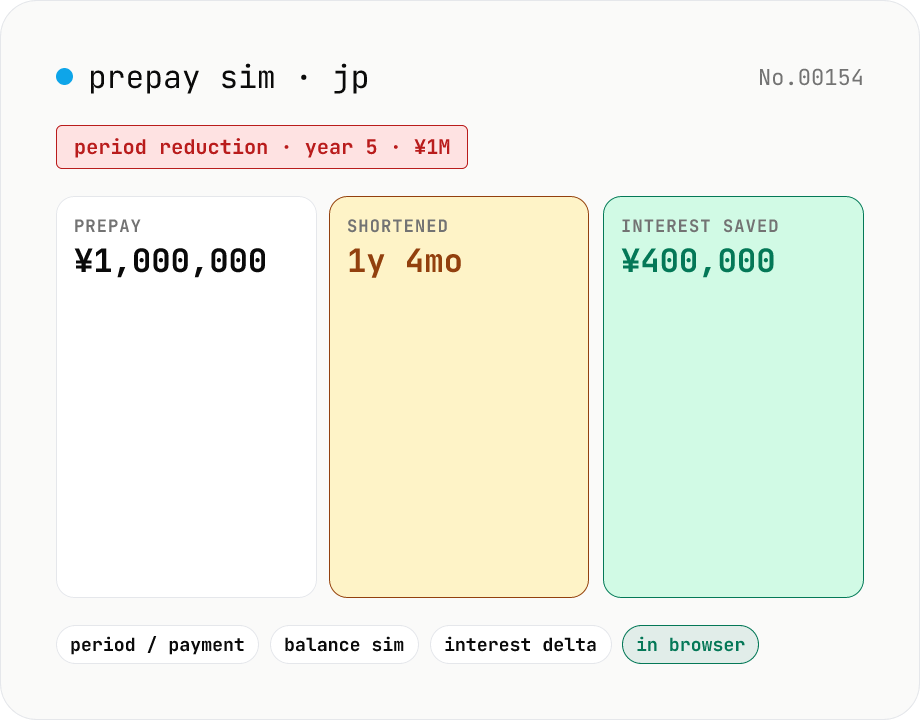

Mortgage prepayment simulator — period-reduction vs payment-reduction

Estimate interest savings from prepaying part of a Japanese mortgage. Plug in the original principal, rate, and term plus the prepayment amount and timing (year), and the tool compares the two prepayment styles: period-reduction (keep monthly payment, shorten the loan) vs payment-reduction (keep the original end date, lower the monthly payment). Equal-payment amortization is assumed. Runs entirely in your browser — loan details never leave the device.

How to use

Pick the prepayment style (period-reduction or payment-reduction), then enter principal, annual rate, term (1–50 years), the prepayment amount, and when you'll make it (year-end of year X). Click Estimate prepayment to see (1) the balance before and after the prepay, (2) a side-by-side comparison of monthly payment, total months and total interest for the baseline vs. the prepay scenario, (3) months shortened (period) or monthly payment change (payment), and (4) the interest savings in either case. Equal-payment amortization is assumed.

FAQ

- Period-reduction vs payment-reduction — which saves more?

- For the same prepayment amount and timing, **period-reduction usually saves more interest**. Payment-reduction is easier on monthly cash flow but produces smaller interest savings. Note that period-reduction can shorten the remaining term below the 10-year minimum for the housing-loan tax credit — be careful if you're early in a credit period.

- Does timing matter?

- Yes — earlier is better. Interest accrues on the balance, so prepaying when the balance is highest (early years) cuts far more future interest. Compare prepayments at year 1, 5, 10, 20 to see the gap.

- Are prepayment fees modelled?

- No — only the interest savings. Banks charge JPY 10k–30k for in-branch prepayments (often free on the web). Small prepayments through a paid channel can be net-negative; check the fee separately.

- What if the prepayment exceeds the balance?

- That's a full payoff. The tool requires the amount to be smaller than the balance at the prepay date; for a full payoff scenario, run loan-calc to find the exact balance at that month and use that amount.

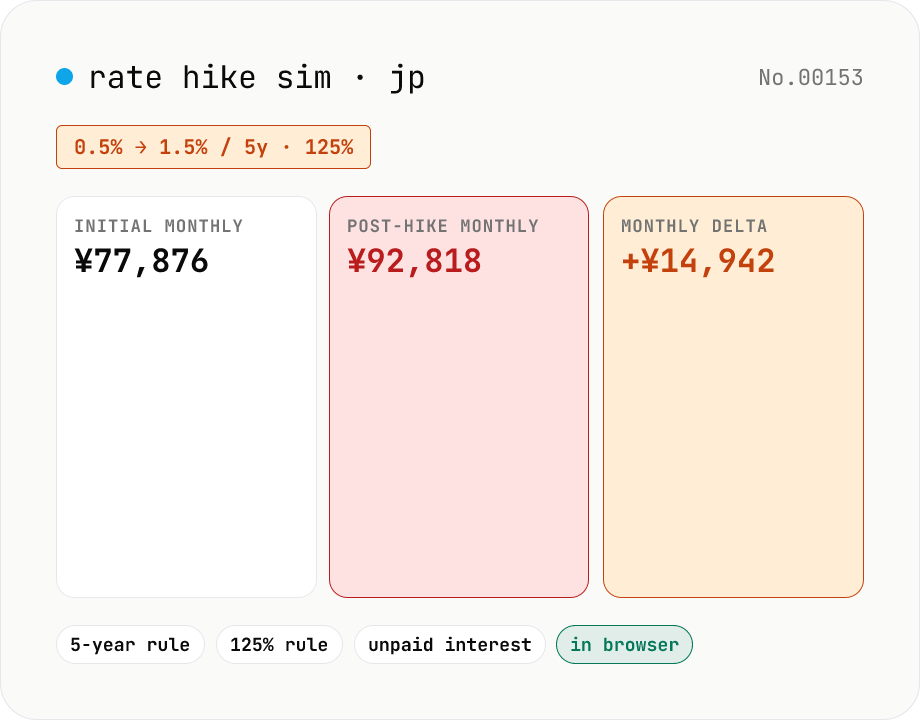

- Floating rate?

- The tool treats the rate as flat for the whole term. For 'prepay after a rate hike' scenarios, run mortgage-floating-jp first to land the new monthly payment, then re-run this tool with the new rate.

- Bonus-payment combinations?

- This tool doesn't model bonus payments. If you have a bonus-blended schedule, derive the effective monthly equivalent in loan-calc first, or run the bonus portion separately.

- How does it interact with the mortgage tax credit?

- Period-reduction prepayments that drop the remaining term below 10 years invalidate the credit. The usual pattern is to finish the credit window first (13 years for new builds) before doing aggressive period-reductions. Use mortgage-deduction-jp to estimate the credit impact separately.

- Is my input uploaded?

- No. Everything runs in your browser — principal and prepayment figures never leave the device.

Related tools

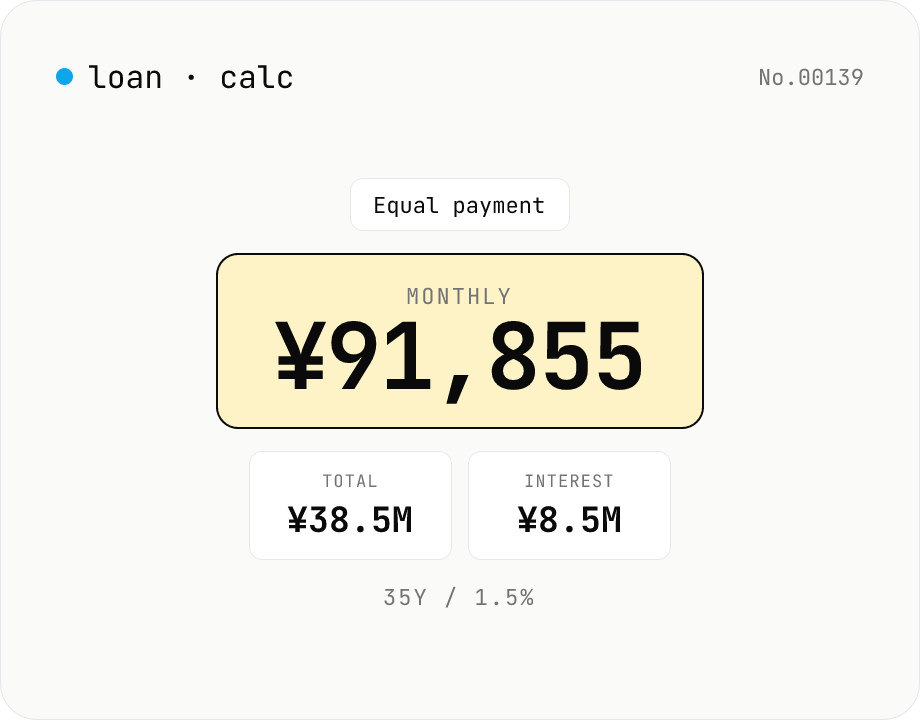

Loan repayment calculator — equal payment & equal principal table

Simulate mortgage, auto, and student-loan repayments under both equal-payment and equal-principal schedules. Enter principal, annual rate, and term to see the monthly payment, total interest, total paid, and a full amortization table. Everything runs in your browser — no loan or income data is uploaded.

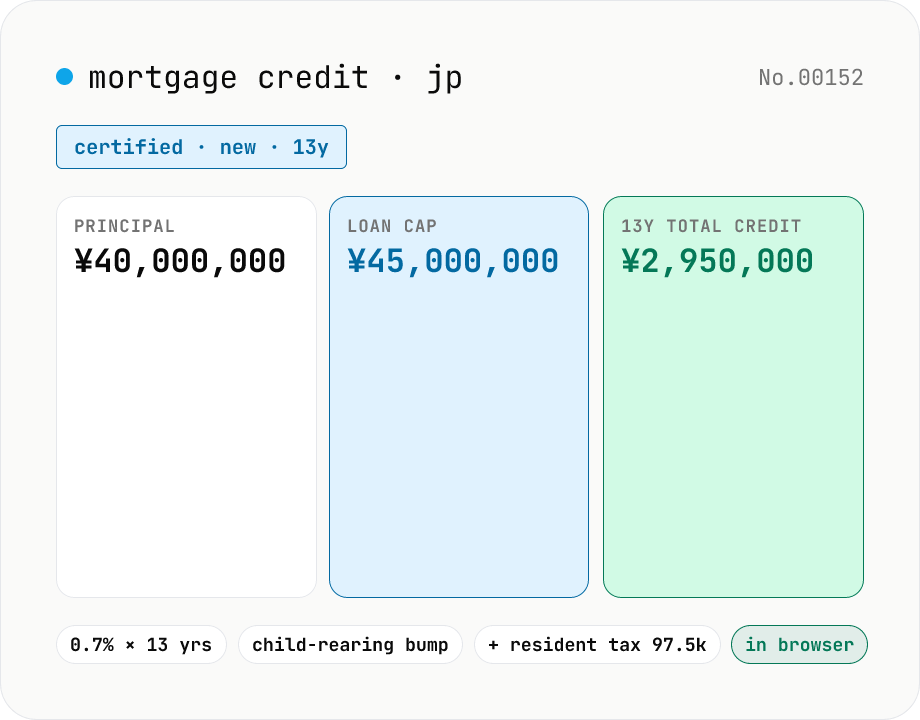

Japan mortgage tax credit estimator — 2024–25 caps, 13-year 0.7%

Estimate the Japanese housing-loan tax credit for 2024 / 2025 occupancy. Borrow caps depend on the property class — new build (LTQ / ZEH / energy-code / other) or existing (energy-class / other) — and on whether the household qualifies as 'child-rearing or young couple' for the higher cap. The tool runs an equal-payment amortization, applies the cap to each year-end balance, multiplies by 0.7%, and stretches over 13 years (new) or 10 years (existing). Any unused income-tax credit spills into the resident-tax credit (JPY 97,500 / year max). Runs entirely in your browser — loan details never leave the device.

Floating-rate mortgage simulator — 5-year / 125% rule support

Simulate a 'rate hike at year X to Y%' scenario for a Japanese floating-rate mortgage. Enter the original rate, term, hike timing, and post-hike rate to compare the no-hike baseline against the post-hike scenario — monthly payment, total interest, total paid. The 5-year rule (monthly payment frozen for 5 years after the hike) and the 125% rule (the new monthly is capped at 1.25× the previous monthly at the 5-year review) are optional toggles, with any resulting unpaid interest surfaced separately. Runs entirely in your browser — loan figures never leave the device.

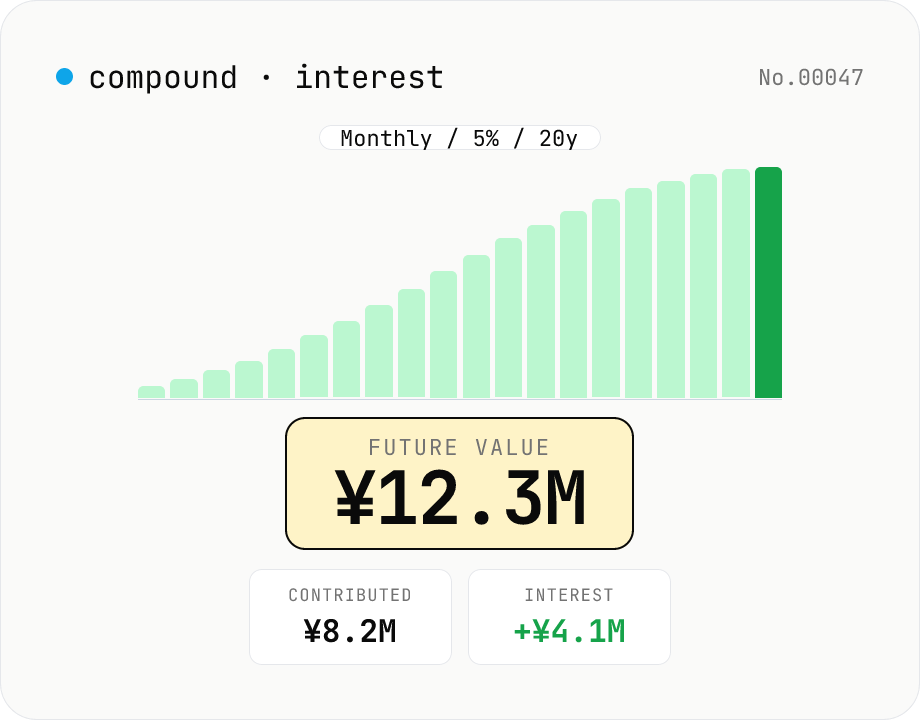

Compound interest calculator — lump-sum & monthly contribution

Project the future value of an investment compounded over time. Supports three modes: principal only, monthly contributions, or annual contributions. Great for simulating Tsumitate NISA / iDeCo / certificates of deposit. Year-by-year balances can be exported as CSV. Principal, rate, and term stay in your browser — nothing is uploaded.