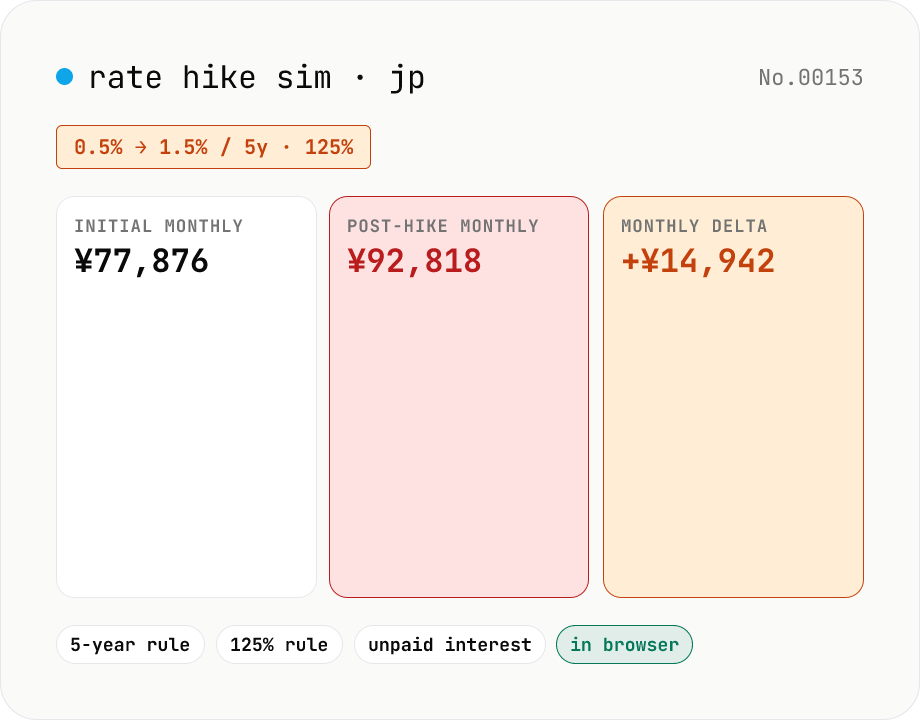

Floating-rate mortgage simulator — 5-year / 125% rule support

Simulate a 'rate hike at year X to Y%' scenario for a Japanese floating-rate mortgage. Enter the original rate, term, hike timing, and post-hike rate to compare the no-hike baseline against the post-hike scenario — monthly payment, total interest, total paid. The 5-year rule (monthly payment frozen for 5 years after the hike) and the 125% rule (the new monthly is capped at 1.25× the previous monthly at the 5-year review) are optional toggles, with any resulting unpaid interest surfaced separately. Runs entirely in your browser — loan figures never leave the device.

How to use

Enter principal, initial annual rate, term (1–50 years), the post-hike rate, and the hike timing (years after origination). Optionally toggle the 5-year rule and the 125% rule, then click Run scenario to see (1) the no-hike baseline, (2) the post-hike scenario, (3) deltas for monthly payment, total interest, total paid, and (4) any unpaid interest. A red note appears when the 125% cap is binding.

FAQ

- What is the 5-year rule?

- Standard JP convention for equal-payment floating loans: **the monthly payment is frozen for 5 years after a rate change**. If interest grows beyond the monthly figure, the shortfall accumulates as unpaid interest added to the balance. Toggle this on to freeze the monthly for 60 months after the hike.

- What is the 125% rule?

- At the 5-year review boundary, the new monthly is **capped at 1.25× the prior monthly**. It prevents a sudden 2–3× jump in monthly payments. Toggle it on (in addition to the 5-year rule) and any computed monthly above 1.25× is held at the cap, with the shortfall logged as unpaid interest.

- How is unpaid interest settled?

- Practice varies by bank. The most common is a lump sum at the final payment; some banks spread the shortfall across the new fuller monthly. This tool assumes 'lump sum at final payment'. For large balances, talk to your lender early.

- When does the cap actually bind?

- Shorter remaining term + larger rate jumps. Example: JPY 30M / 35 years / 1.0% → 3.0% after 5 years: amortising JPY 26.6M over 30 years at 3% needs ~¥112k/month, which is 1.33× the original ¥84k → capped at ¥105k.

- What if I turn off the 5-year rule?

- The monthly payment switches to the post-hike value at the hike month itself (which is NOT how most JP banks operate, but useful for worst-case monthly impact or for equal-principal contracts that don't have the 5-year freeze).

- Why only one hike?

- Floating-rate loans actually adjust every 6 months. Modelling that exactly would require a long rate-path input. This tool stays simple — pick the single worst-case 'rate steps up' moment. Run it multiple times with different timings to explore scenarios.

- Can I combine this with prepayments?

- Not in this tool. Use mortgage-prepay-jp for the prepayment side; treat the post-hike rate from here as the new annual rate there.

- Is my input uploaded?

- No. Everything runs in your browser — loan figures never leave the device.

Related tools

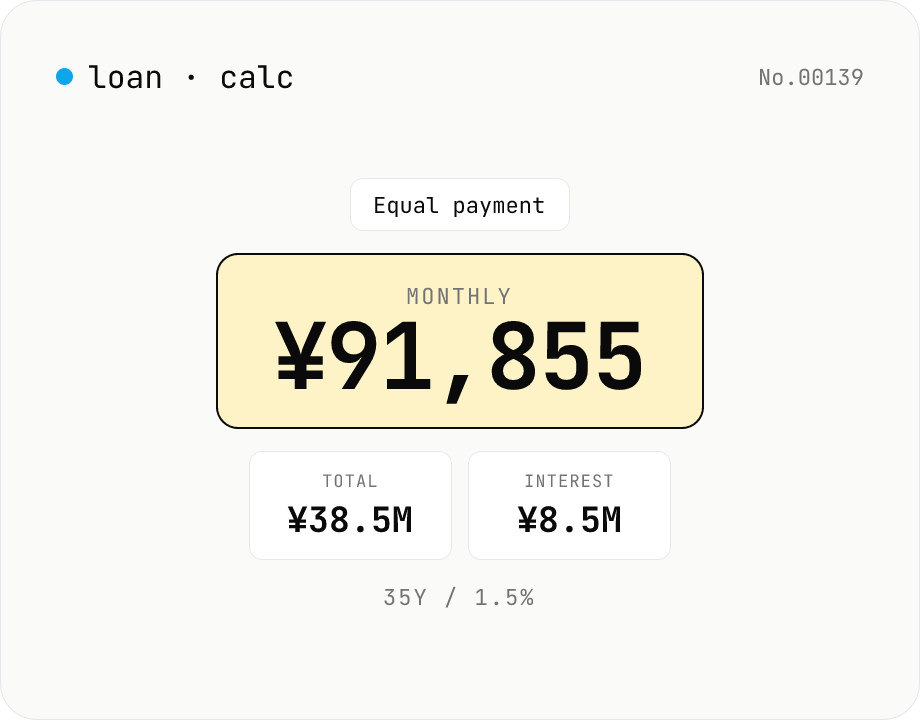

Loan repayment calculator — equal payment & equal principal table

Simulate mortgage, auto, and student-loan repayments under both equal-payment and equal-principal schedules. Enter principal, annual rate, and term to see the monthly payment, total interest, total paid, and a full amortization table. Everything runs in your browser — no loan or income data is uploaded.

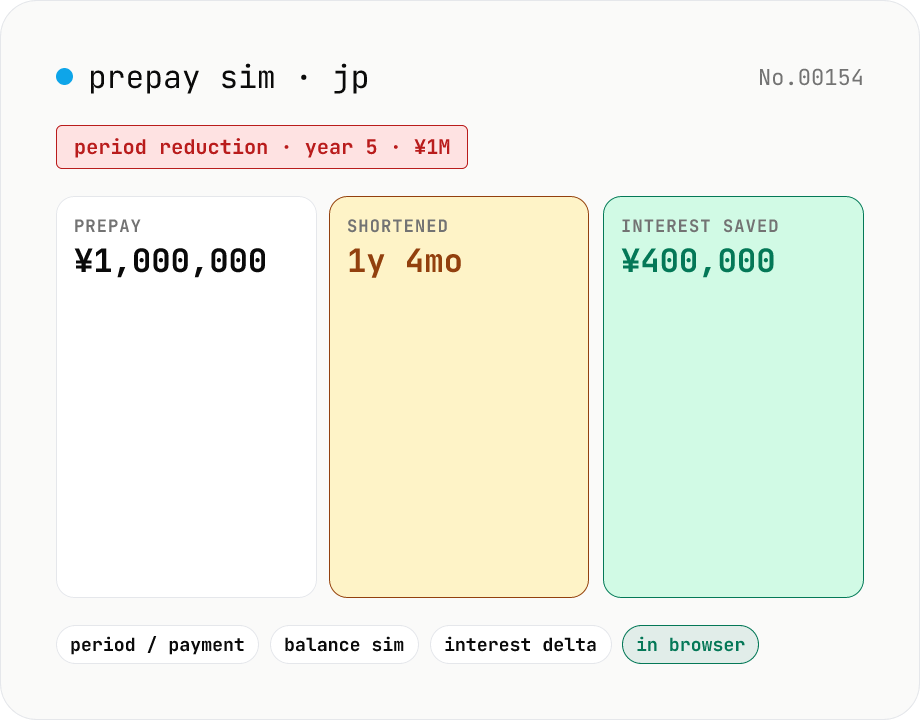

Mortgage prepayment simulator — period-reduction vs payment-reduction

Estimate interest savings from prepaying part of a Japanese mortgage. Plug in the original principal, rate, and term plus the prepayment amount and timing (year), and the tool compares the two prepayment styles: period-reduction (keep monthly payment, shorten the loan) vs payment-reduction (keep the original end date, lower the monthly payment). Equal-payment amortization is assumed. Runs entirely in your browser — loan details never leave the device.

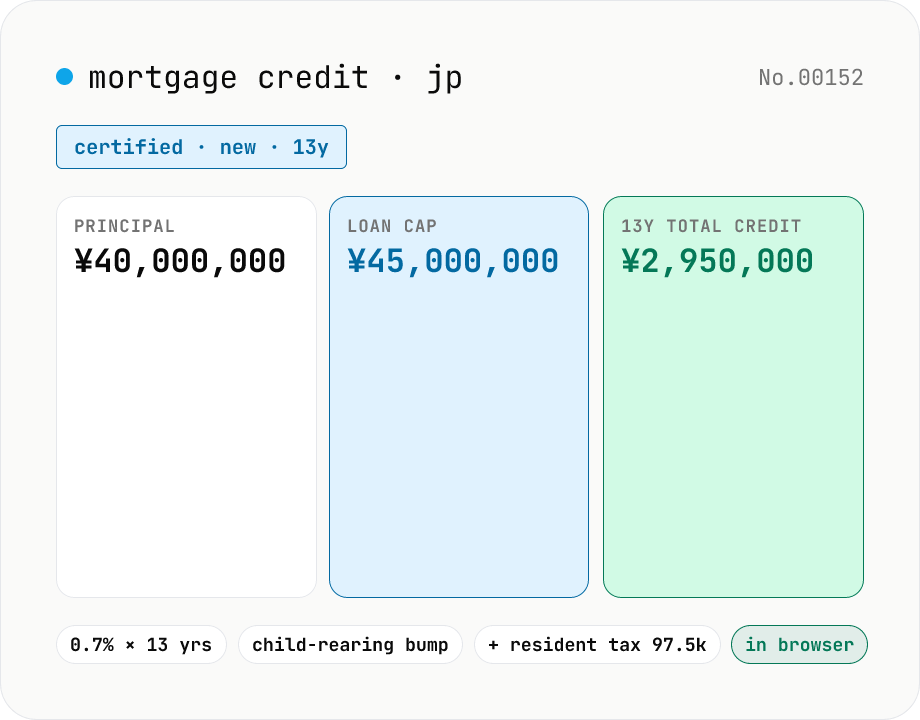

Japan mortgage tax credit estimator — 2024–25 caps, 13-year 0.7%

Estimate the Japanese housing-loan tax credit for 2024 / 2025 occupancy. Borrow caps depend on the property class — new build (LTQ / ZEH / energy-code / other) or existing (energy-class / other) — and on whether the household qualifies as 'child-rearing or young couple' for the higher cap. The tool runs an equal-payment amortization, applies the cap to each year-end balance, multiplies by 0.7%, and stretches over 13 years (new) or 10 years (existing). Any unused income-tax credit spills into the resident-tax credit (JPY 97,500 / year max). Runs entirely in your browser — loan details never leave the device.

Compound interest calculator — lump-sum & monthly contribution

Project the future value of an investment compounded over time. Supports three modes: principal only, monthly contributions, or annual contributions. Great for simulating Tsumitate NISA / iDeCo / certificates of deposit. Year-by-year balances can be exported as CSV. Principal, rate, and term stay in your browser — nothing is uploaded.