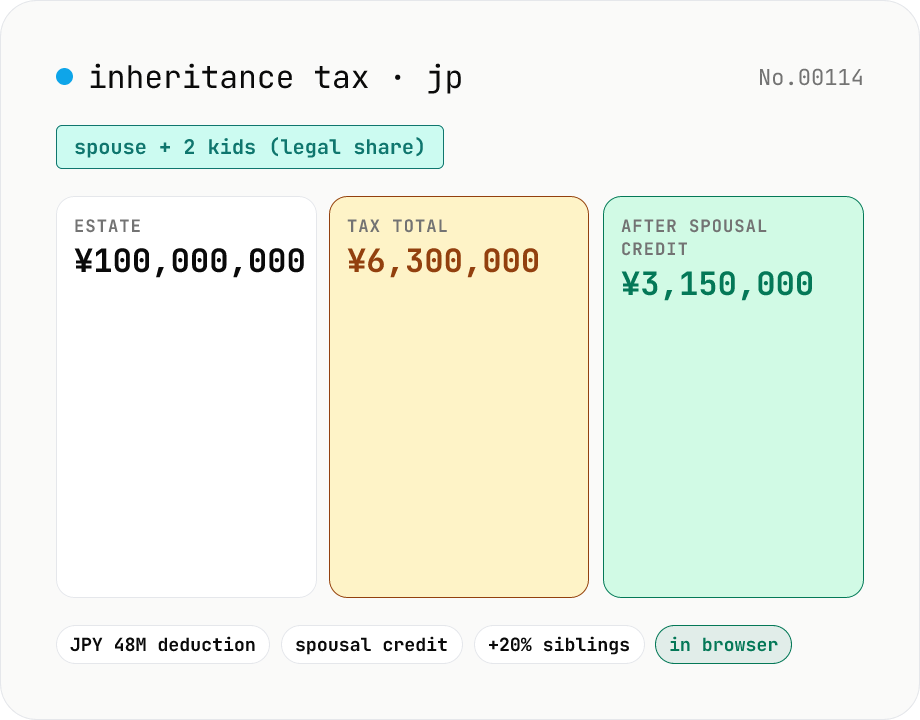

Japan inheritance tax estimator — basic deduction, legal shares, spousal credit

Enter the estate value and your heir composition (spouse yes/no, child / parent / sibling counts) for a Japanese inheritance tax estimate. The tool applies: the JPY 30M + JPY 6M × heirs basic deduction, the per-heir taxable amount from the legal-share split, the NTA quick-deduction tables (8 brackets, up to 55%), the spousal tax credit (zero tax for a spouse taking exactly the legal share), and the 20% surcharge on siblings. Heir-class priority (children → parents → siblings) is detected automatically. Runs entirely in your browser — estate figures never leave the device.

How to use

Enter the estate value (after debts and funeral costs are subtracted from the taxable value), pick whether there's a surviving spouse, then enter the child / parent / sibling counts. Click Estimate tax to see (1) the basic deduction (JPY 30M + 6M × legal heirs), (2) the taxable estate, (3) the per-heir taxable amount from the legal-share split, (4) the inheritance tax total, (5) the spousal credit (which zeroes the spouse's tax in the legal-share scenario), and (6) the 20% surcharge applied to sibling heirs. Heir-class priority (children → parents → siblings) is auto-detected — children block parents and siblings, etc.

FAQ

- Who counts as a legal heir?

- The surviving spouse is always an heir. Plus: tier 1 = children (or their substitutes), tier 2 = lineal ascendants (parents, grandparents), tier 3 = siblings. Higher tiers block lower ones — if there are children, parents and siblings drop out; if there are no children but parents survive, siblings drop out.

- How are legal shares computed?

- Spouse + children: spouse 1/2, children 1/2 (split evenly). Spouse + parents: spouse 2/3, parents 1/3. Spouse + siblings: spouse 3/4, siblings 1/4. Spouse only: spouse 100%. No spouse: divide evenly within the active tier. The tool follows this automatically.

- What is the basic deduction?

- JPY 30M + JPY 6M × number of legal heirs. E.g. spouse + 2 children = 30 + 6 × 3 = JPY 48M. Estates below the basic deduction pay no inheritance tax and generally do not need to file. The 2015 reform tightened this from the earlier 50M + 10M × heirs threshold, so a house in central Tokyo now often triggers a filing.

- What is the spousal tax credit?

- The surviving spouse pays no inheritance tax on a taxable share up to the greater of JPY 160M or the spouse's legal share (No.4158). This tool assumes the spouse takes exactly the legal share, so the spouse's net tax is always zero. If the spouse actually takes a different proportion in the estate division agreement, recompute manually.

- Why are siblings hit with a 20% surcharge?

- Heirs who are neither the spouse nor a first-degree blood relative (children, parents) get their computed tax bumped up by 20% (No.4157). Siblings qualify, as do (substitute) grandchildren who aren't a child's biological child. This tool applies the surcharge to the sibling group only.

- How are adopted children handled?

- For deduction-counting purposes (basic deduction, life-insurance non-taxable cap, etc.), the number of adopted children that count is capped at 1 if any biological child exists, or 2 if none. This tool does NOT enforce that cap — enter the post-cap number yourself.

- What about debts / funeral costs / lifetime gifts?

- Subtract debts and funeral costs from the gross estate before entering. Gifts within 3–7 years before death are added back into the estate; this tool assumes they are already included in your input. Consult a tax advisor for the exact treatment.

- And the small-residential-land special exemption?

- Up to 330㎡ residential land qualifies for an 80% valuation cut (and up to 400㎡ business land for the same cut). Apply the exemption first, then enter the post-exemption estate value here. Eligibility / area allocation goes through a tax advisor.

- Is my input uploaded?

- No. Everything runs in your browser — estate figures and heir details never leave the device.

Related tools

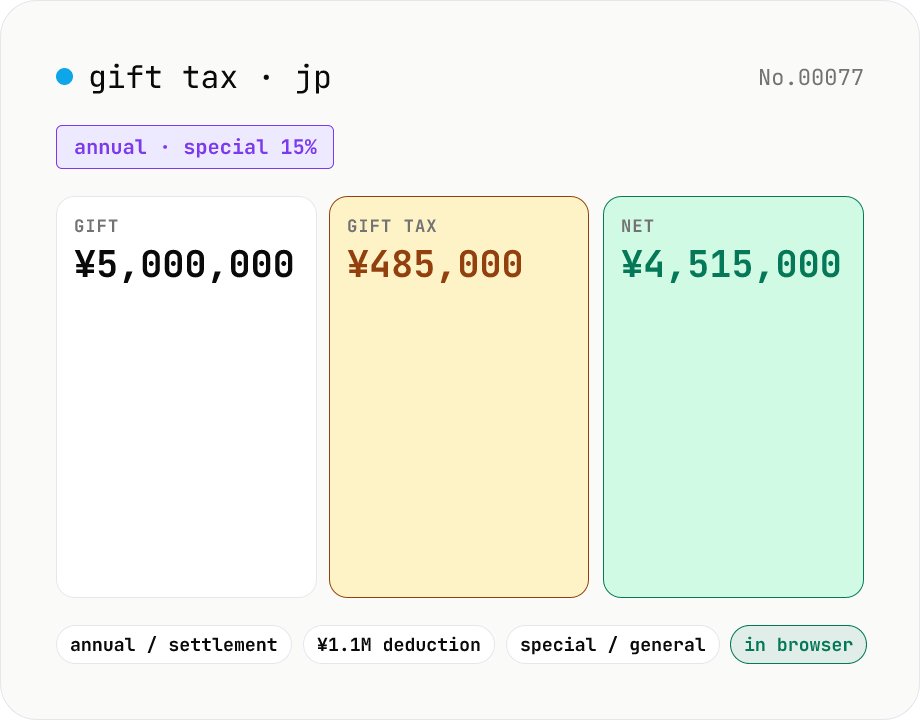

Japan gift tax estimator — annual / settlement methods (2024 reform)

Enter the gift amount for the year and estimate the Japanese gift tax under the annual (暦年課税) method. Switch between the special rate (lineal descendants aged 18+) and the general rate (everyone else). The JPY 1.1M annual basic deduction and the NTA rate / quick-deduction tables are applied. The settlement-at-inheritance method (相続時精算課税) is also supported, reflecting the 2024 reform that added a separate JPY 1.1M annual deduction on top of the cumulative JPY 25M lifetime allowance (20% flat above). Runs entirely in your browser — figures never leave the device.

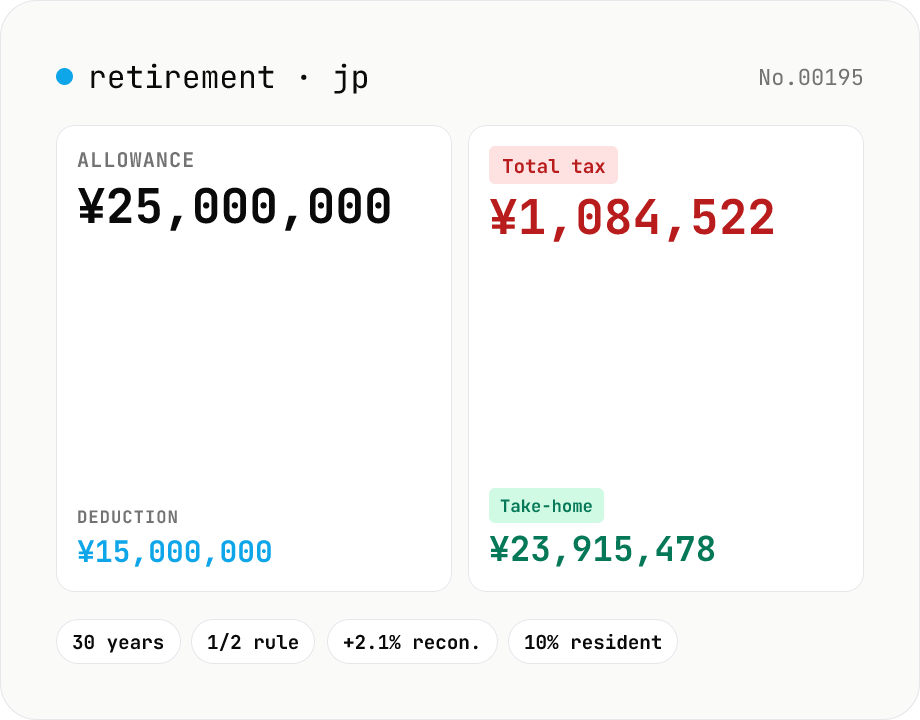

Japanese retirement-allowance tax estimator — 退職所得控除 calculator

Enter your retirement allowance and tenure to estimate the retirement-income deduction (退職所得控除), taxable amount with the 1/2 rule, income tax, special reconstruction tax, resident tax and net take-home. Supports the short-tenure variants (短期退職手当等 / 特定役員退職手当等) and the disability bump. Runs entirely inside your browser — figures never leave your device.

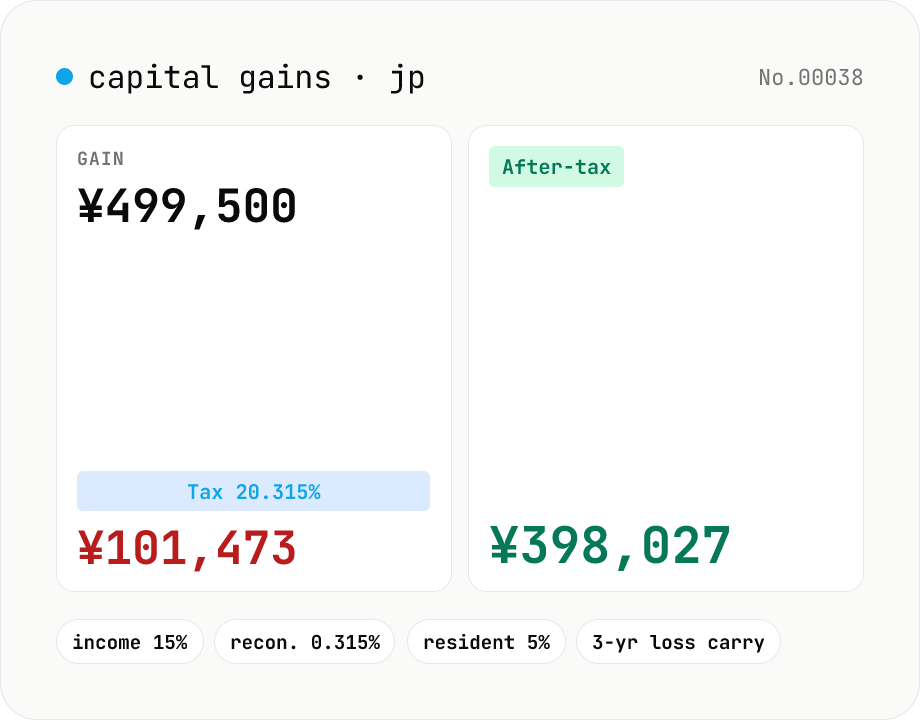

Japanese capital-gains tax (20.315%) — stock-sale net calculator

Estimate the 20.315% Japanese tax on listed-stock and mutual-fund capital gains (income tax 15% + 0.315% reconstruction surtax + 5% resident tax). Enter sale proceeds, acquisition cost (incl. buy-side fees) and sell-side expenses; the tool returns the gain, each tax line and the after-tax take-home. Losses display zero tax and a note about the 3-year carry-over deduction. Excludes NISA / iDeCo tax-free balances. Runs entirely in your browser — your figures never leave the device.

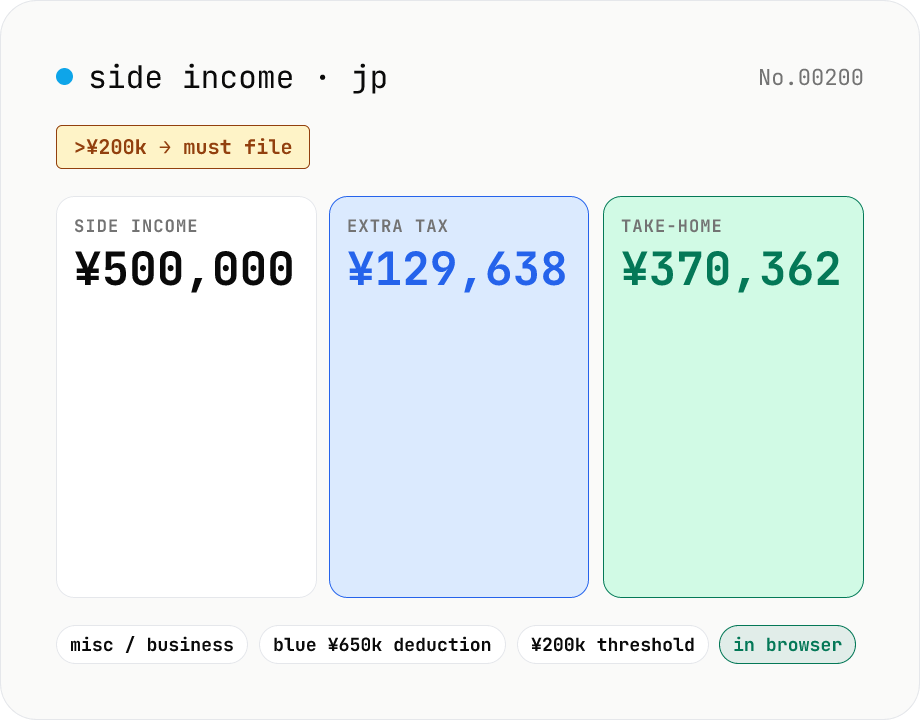

Japan side-income tax estimator — the 200k-yen filing threshold

Plug in your salary, side-job revenue and expenses to estimate the extra income tax, reconstruction surtax and resident tax — plus net take-home — that the side gig adds on top of a salaried job. Detects the JPY 200,000/year filing threshold (no income tax under it, but resident tax filing is still required). Switch between miscellaneous and business income; business + blue-return adds the JPY 650,000 deduction. Runs entirely in your browser — figures never leave the device.