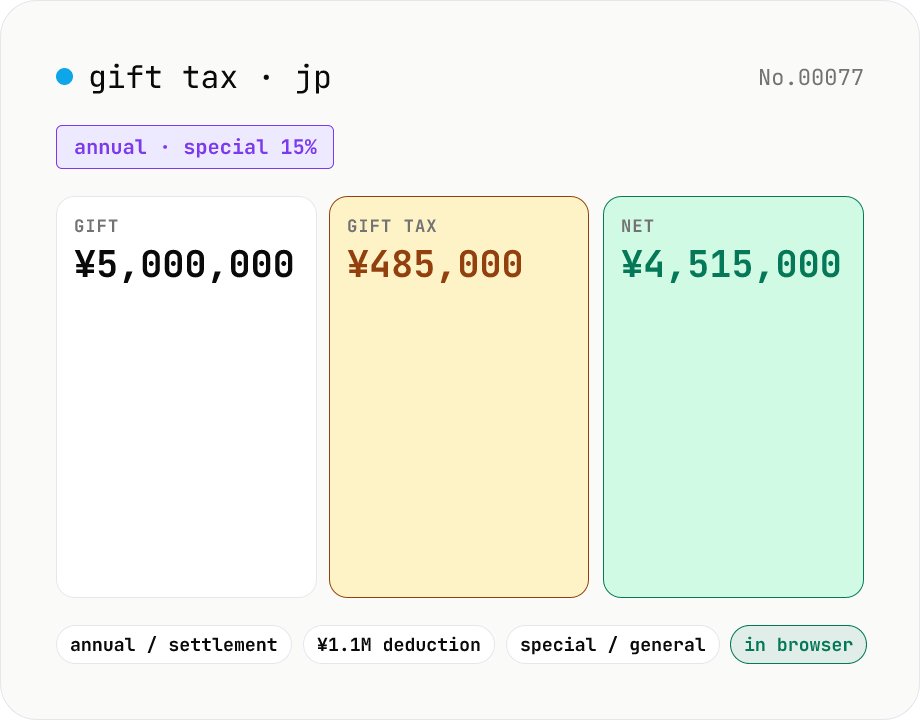

Japan gift tax estimator — annual / settlement methods (2024 reform)

Enter the gift amount for the year and estimate the Japanese gift tax under the annual (暦年課税) method. Switch between the special rate (lineal descendants aged 18+) and the general rate (everyone else). The JPY 1.1M annual basic deduction and the NTA rate / quick-deduction tables are applied. The settlement-at-inheritance method (相続時精算課税) is also supported, reflecting the 2024 reform that added a separate JPY 1.1M annual deduction on top of the cumulative JPY 25M lifetime allowance (20% flat above). Runs entirely in your browser — figures never leave the device.

How to use

Pick the taxation method (annual / settlement). For the annual method, pick the recipient category (special rate for lineal descendants aged 18+, general rate for everyone else) and enter the total gifts received in the calendar year. Click Estimate tax to see the taxable amount after the JPY 1.1M annual deduction, the applied bracket rate, quick-deduction, gift tax due, recipient net and effective rate. For the settlement method, also enter the cumulative special allowance already used in prior years. The 2024 reform adds a separate JPY 1.1M annual deduction; the excess consumes up to JPY 25M of the lifetime special allowance, with 20% flat applied beyond.

FAQ

- What's the difference between the annual and settlement methods?

- Annual is the default — JPY 1.1M tax-free each year, progressive rates above. Settlement is opt-in, restricted to gifts from parents/grandparents (≥ 60) to children/grandchildren (≥ 18); up to JPY 25M cumulative is tax-free, 20% flat above. The catch: gifts under the settlement method are added back into the estate at the donor's death and taxed again under inheritance tax (so it defers, not eliminates, taxation). The 2024 reform added a separate JPY 1.1M annual deduction to the settlement method — that part is NOT added back at death.

- Special vs. general rate?

- Special: lower rate table, applies to gifts from grandparents/parents to lineal descendants (child/grandchild) aged 18+ (measured on Jan 1 of the gift year). General: higher rate table, applies to sibling-to-sibling, spousal, child's-spouse and gifts to minor descendants. For example, on a JPY 5M taxable amount: special is JPY 530k (15%) vs. general at JPY 780k (20%) — a JPY 250k spread.

- Multiple donors in one year?

- Under the annual method, sum every gift received in the calendar year before subtracting the JPY 1.1M (the deduction is per recipient, not per donor). E.g. JPY 800k from your father + JPY 800k from your mother = JPY 1.6M, leaving JPY 500k taxable. Gifts under the settlement method are tracked separately — its JPY 1.1M annual deduction is in addition to the annual-method's.

- Do I need to file?

- Annual method: yes if the taxable amount > 0 (i.e. gifts > JPY 1.1M). Settlement method (post-2024 reform): no filing if the year's gifts ≤ JPY 1.1M after the initial 'settlement election' is filed. A filing IS required for any year the lifetime special allowance is consumed.

- How does the JPY 20M spousal deduction work?

- For couples married 20+ years gifting residential real-estate (or funds to acquire it), up to JPY 20M can be deducted on top of the JPY 1.1M annual deduction. **Not modelled here** — subtract JPY 20M manually before plugging the amount into this tool under 'general rate'. Same applies to the housing-acquisition, education and marriage/childcare fund lump-sum exemptions.

- What if I exceed the JPY 25M lifetime allowance?

- 20% flat tax on the excess. E.g. JPY 20M already used + JPY 10M this year: subtract the JPY 1.1M annual, leaving JPY 8.9M; consume the last JPY 5M of the allowance, leaving JPY 3.9M × 20% = JPY 780k gift tax. The gift tax paid is credited (potentially refunded) against the estate tax due at the donor's death.

- How do I prove the gift happened?

- This tool only computes the tax — it does not advise on filing. Generally: (1) sign a written gift agreement, (2) use a bank transfer (no cash hand-off), (3) make sure the recipient actually controls the receiving account. Check with a tax advisor for the specifics.

- Is my input uploaded?

- No. The calculation runs entirely in your browser, so gift amounts never leave the device.

Related tools

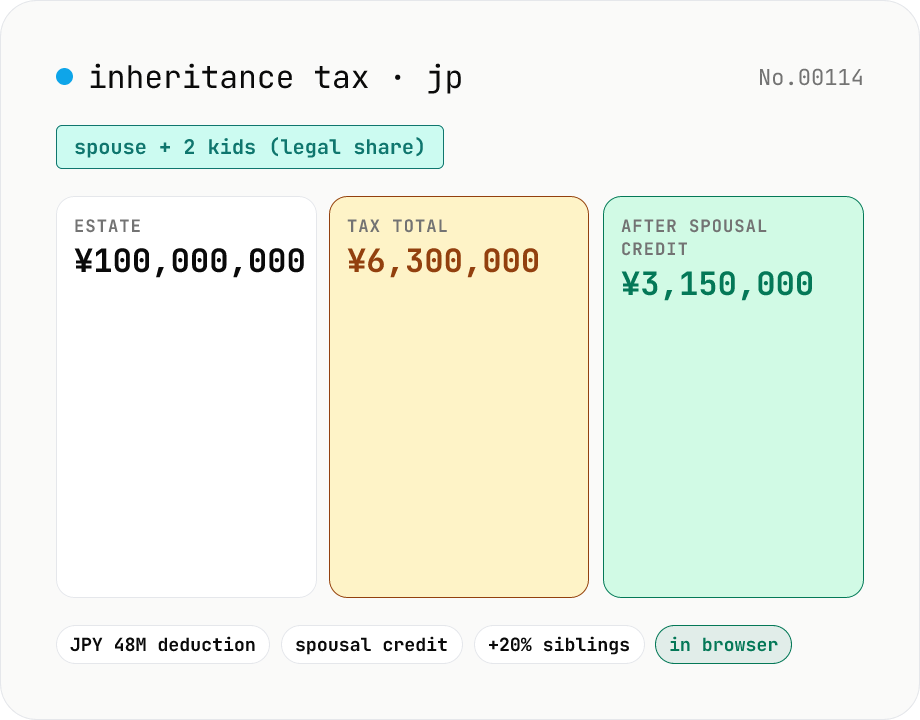

Japan inheritance tax estimator — basic deduction, legal shares, spousal credit

Enter the estate value and your heir composition (spouse yes/no, child / parent / sibling counts) for a Japanese inheritance tax estimate. The tool applies: the JPY 30M + JPY 6M × heirs basic deduction, the per-heir taxable amount from the legal-share split, the NTA quick-deduction tables (8 brackets, up to 55%), the spousal tax credit (zero tax for a spouse taking exactly the legal share), and the 20% surcharge on siblings. Heir-class priority (children → parents → siblings) is detected automatically. Runs entirely in your browser — estate figures never leave the device.

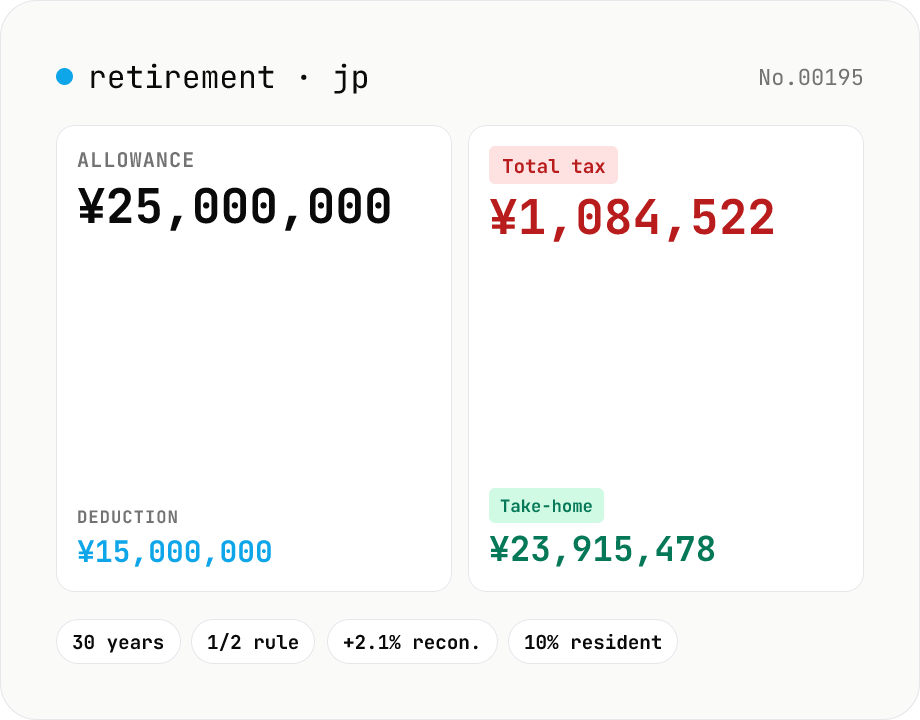

Japanese retirement-allowance tax estimator — 退職所得控除 calculator

Enter your retirement allowance and tenure to estimate the retirement-income deduction (退職所得控除), taxable amount with the 1/2 rule, income tax, special reconstruction tax, resident tax and net take-home. Supports the short-tenure variants (短期退職手当等 / 特定役員退職手当等) and the disability bump. Runs entirely inside your browser — figures never leave your device.

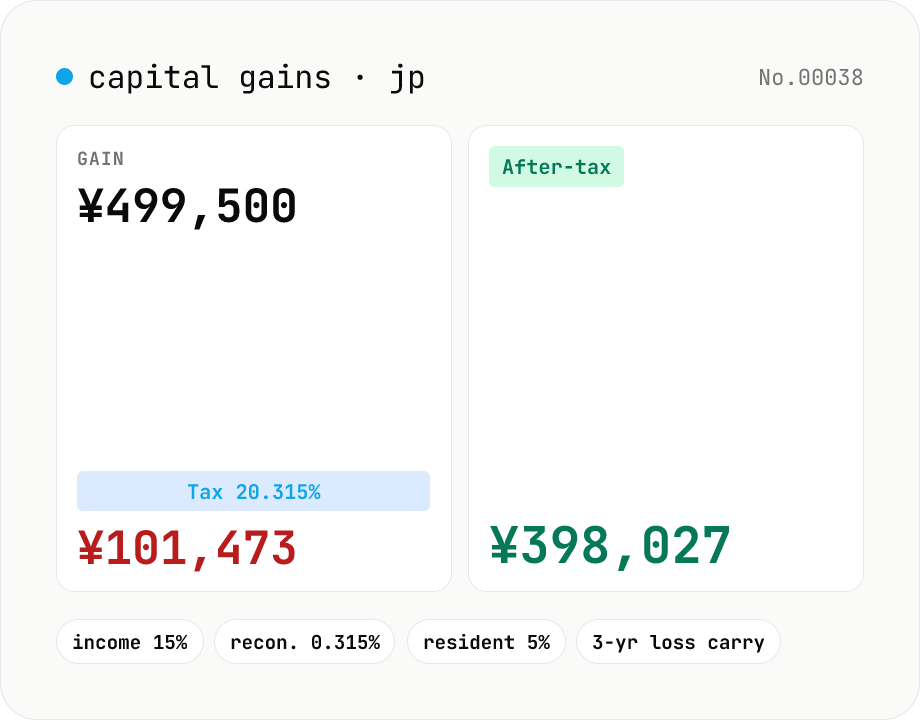

Japanese capital-gains tax (20.315%) — stock-sale net calculator

Estimate the 20.315% Japanese tax on listed-stock and mutual-fund capital gains (income tax 15% + 0.315% reconstruction surtax + 5% resident tax). Enter sale proceeds, acquisition cost (incl. buy-side fees) and sell-side expenses; the tool returns the gain, each tax line and the after-tax take-home. Losses display zero tax and a note about the 3-year carry-over deduction. Excludes NISA / iDeCo tax-free balances. Runs entirely in your browser — your figures never leave the device.

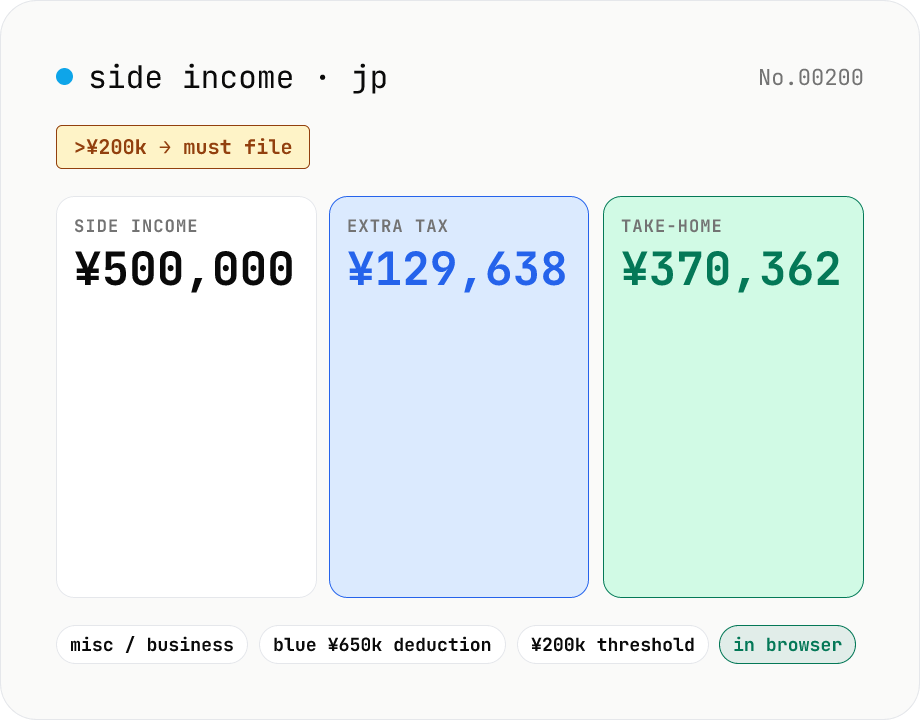

Japan side-income tax estimator — the 200k-yen filing threshold

Plug in your salary, side-job revenue and expenses to estimate the extra income tax, reconstruction surtax and resident tax — plus net take-home — that the side gig adds on top of a salaried job. Detects the JPY 200,000/year filing threshold (no income tax under it, but resident tax filing is still required). Switch between miscellaneous and business income; business + blue-return adds the JPY 650,000 deduction. Runs entirely in your browser — figures never leave the device.